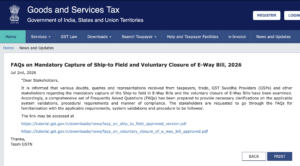

GSTN has issued an important advisory dated 21 May 2026 regarding upcoming enhancements in the E-Way Bill (EWB) Portal. These proposed changes are aimed at improving:

- data quality,

- invoice traceability,

- operational transparency,

- and fraud prevention in the GST ecosystem.

The advisory introduces two major proposed changes in the EWB system:

- Mandatory reporting of “Ship-To GSTIN” in Bill-To Ship-To transactions

- Introduction of E-Way Bill Closure functionality

These changes may require ERP modifications, software updates, and process-level adjustments by taxpayers, transporters, and GST software providers.

Click here to read full advisory

Why GSTN is Introducing These Changes

GSTN has stated that these enhancements are part of its ongoing efforts towards:

- strengthening data integrity,

- improving tracking of goods movement,

- enabling better reconciliation,

- and reducing misuse of E-Way Bills.

With increasing data analytics under GST, authorities are now focusing heavily on:

- actual consignee tracking,

- movement verification,

- invoice matching,

- and prevention of fake billing practices.

1. Mandatory “Ship-To GSTIN” in Bill-To Ship-To Transactions

What is a Bill-To Ship-To Transaction?

In many business models:

- invoice is raised to one person (“Bill-To” party),

- but goods are delivered to another location/entity (“Ship-To” party).

Example:

- Head office places order,

- goods directly delivered to branch office or customer location.

Currently, taxpayers often mention:

- Bill-To details,

- and shipping address,

but Ship-To GSTIN may not always be captured properly.

New Proposed Change

GSTN now proposes mandatory capture of:

“Ship-To GSTIN”

in Bill-To Ship-To transactions on the EWB portal.

This means:

- taxpayers will now have to provide GSTIN of the actual consignee/location where goods are delivered.

Objective Behind This Change

GSTN wants to:

- improve end-to-end traceability of goods,

- accurately identify actual recipient,

- strengthen audit trail,

- and reduce fake movement transactions.

This change will help authorities:

- match invoice data,

- track actual goods destination,

- and verify GST compliance more effectively.

Practical Impact on Businesses

This enhancement may significantly impact:

- ERP systems,

- invoicing software,

- logistics integration,

- and EWB APIs.

Businesses using automated EWB generation systems may need:

- software upgrades,

- API mapping changes,

- additional master validations,

- and process modifications.

Sectors Likely to be Highly Impacted

The following sectors frequently use Bill-To Ship-To models and may face major operational changes:

| Sector | Impact |

|---|---|

| FMCG | High |

| E-commerce | High |

| Pharmaceuticals | High |

| Multi-location businesses | High |

| Job work transactions | Moderate |

| Distribution networks | High |

Important Compliance Point

If Ship-To GSTIN becomes mandatory:

- incorrect GSTIN reporting,

- use of invalid consignee GSTIN,

- or mismatch with invoice details

may lead to: - EWB rejection,

- detention risks,

- reconciliation issues,

- or departmental scrutiny.

Businesses should therefore begin reviewing:

- customer master data,

- consignee GSTIN mapping,

- and shipping workflows.

2. Introduction of E-Way Bill Closure Functionality

Another major proposed enhancement is:

EWB Closure Facility

This will allow taxpayers to voluntarily close E-Way Bills under specified situations.

Why is EWB Closure Needed?

Currently, many E-Way Bills remain active even when:

- goods movement never happened,

- shipment got cancelled,

- dispatch failed,

- invoice was cancelled later,

- or transaction became invalid.

In such situations:

- EWB may continue showing as active,

- creating unnecessary compliance risks and data inconsistencies.

What Will the New Closure Facility Do?

The proposed functionality will allow taxpayers to:

- voluntarily close EWB,

- declare non-movement/cancellation scenarios,

- and maintain accurate transport records.

This will improve:

- data accuracy,

- transport audit trail,

- and operational transparency.

Expected Benefits of EWB Closure Feature

1. Better Record Management

Inactive or unused EWBs can be formally closed.

2. Reduced Compliance Risk

Businesses can avoid unnecessary mismatches during audits.

3. Improved Data Accuracy

GSTN databases will better reflect actual goods movement.

4. Lower Litigation Risk

Taxpayers can proactively document cancelled movements.

Possible Scenarios Where Closure May Be Used

The closure facility may become useful in cases like:

- goods not dispatched,

- order cancelled,

- transporter issue,

- invoice cancellation,

- duplicate EWB generated,

- wrong EWB created,

- shipment returned before dispatch,

- or logistics failure.

Detailed operational guidelines are expected from GSTN separately.

System Changes Required by Businesses

Businesses and software providers should start preparing for:

- ERP modifications,

- API changes,

- validation logic updates,

- EWB workflow redesign,

- and master data corrections.

Companies using integrated GST systems should coordinate with:

- ERP vendors,

- GST software providers,

- and API integrators.

Action Points for Taxpayers

GSTN has advised stakeholders to begin preparedness activities.

Businesses should:

- review Bill-To Ship-To processes,

- validate customer GSTIN databases,

- update EWB integration systems,

- train GST teams,

- and monitor future GSTN implementation notifications.

Important Note About Implementation

The advisory currently discusses:

proposed enhancements

along with:

- expected timelines,

- and preparedness requirements.

Detailed implementation procedures and technical specifications are likely to be issued separately by GSTN.

Conclusion

The latest GSTN advisory signals another major step towards deeper automation and traceability in the GST system.

The introduction of:

- mandatory Ship-To GSTIN reporting,

- and EWB Closure functionality

will significantly improve:

- invoice tracking,

- goods movement transparency,

- and GST analytics.

However, these changes may also increase compliance responsibility for businesses using complex supply chains and automated EWB systems.

Taxpayers should proactively review their systems and workflows to ensure smooth compliance once these enhancements become operational on the E-Way Bill portal.

Visit www.cagurujiclasses.com for practical courses