E-Invoicing under GST is not about generating invoices on a portal, but about reporting invoice details to the Invoice Registration Portal (IRP) and obtaining a unique IRN (Invoice Reference Number).

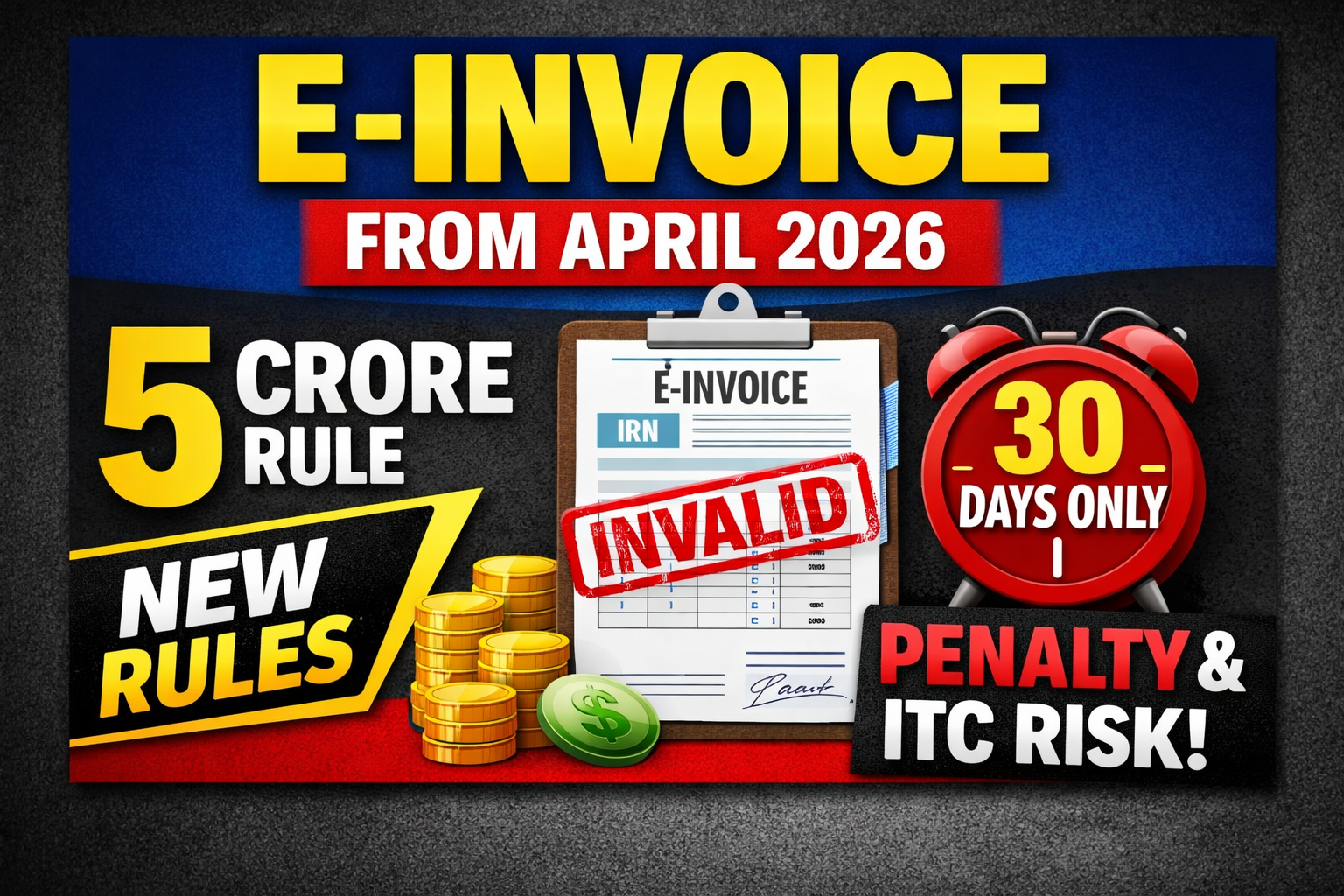

From 1st April 2026, the applicability remains primarily based on turnover threshold, but practical compliance has become stricter due to time limits and ITC implications.

Who is Required to Generate E-Invoice?

Turnover Criteria

E-Invoicing is mandatory for:

👉 Registered persons whose aggregate turnover exceeds ₹5 crore

👉 In any financial year from FY 2017-18 onwards

📌 Important Points

- Turnover is calculated on PAN basis (all GSTINs combined)

- Includes:

- Taxable supplies

- Exempt supplies

- Exports

- Inter-state supplies

🧾 Example 1 (Basic Applicability)

👉 ABC Pvt Ltd turnover:

| Year | Turnover |

|---|---|

| FY 2021-22 | ₹6 Cr |

| FY 2025-26 | ₹3 Cr |

✔ Since turnover exceeded ₹5 Cr in past

➡ E-Invoice is still mandatory in FY 2026-27

If turnover exceeds 5 crore in FY 2025-26 then it is mandatory to start E invoice from 1 April 2026

🧾 Example 2 (PAN Based Calculation)

👉 Mr. X has 2 GSTINs:

- Delhi: ₹3 Cr

- Haryana: ₹3 Cr

👉 Total PAN turnover = ₹6 Cr

➡ E-Invoicing applicable on BOTH GSTINs

Transactions Covered under E Invoicing

✅ Applicable Transactions

- B2B Supplies

- Export supplies

- Supplies to SEZ units/developers

- Deemed exports

- Supplies to Government (B2G)

❌ Not Applicable

- B2C supplies

- NIL rated / non-GST supplies (no invoice required)

🧾 Example 3 (Transaction Level)

👉 A company (eligible for e-invoice) makes:

- Sale to registered dealer → ✅ E-Invoice required

- Sale to consumer → ❌ Not required

⏰ Time Limit for Generating E-Invoice (Very Important)

👉 Applicable to taxpayers with turnover ≥ ₹10 Cr

- Invoice must be uploaded to IRP within 30 days from invoice date

⚠️ Consequence

- After 30 days → IRP will not generate IRN

- Invoice becomes invalid under GST

🧾 Example 4 (Time Limit Impact)

👉 Invoice dated: 1 April 2026

👉 Upload attempted: 5 May 2026

❌ Delay beyond 30 days

➡ IRN cannot be generated

➡ Invoice becomes invalid

➡ Buyer may lose ITC

🚫 5. Persons Exempt from E-Invoicing

Even if turnover exceeds ₹5 Cr, the following are not required:

- Banking companies / NBFCs

- Insurance companies

- Goods Transport Agencies (GTA)

- Passenger transport services

- Cinema exhibition (multiplex)

- Government departments / local authorities

🧾 Example 5 (Exemption)

👉 XYZ Bank with turnover ₹500 Cr

➡ Still NOT required to generate e-invoice

⚠️ Consequences of Non-Compliance

If e-invoice is not generated where applicable:

👉 Invoice will be treated as invalid

Practical Impact:

- ❌ No valid tax invoice

- ❌ ITC may be denied to buyer

- ❌ Penalty under GST

- ❌ Risk of litigation

🧾 Example 6 (Real Risk Case)

👉 Supplier issues normal invoice without IRN

➡ Buyer claims ITC

🔴 Department may deny ITC saying:

“Invoice is invalid as e-invoice not generated”

📉 Evolution of E-Invoice Threshold

| Effective Date | Threshold |

|---|---|

| Oct 2020 | ₹500 Cr |

| Jan 2021 | ₹100 Cr |

| Apr 2022 | ₹20 Cr |

| Oct 2022 | ₹10 Cr |

| Aug 2023 onwards | ₹5 Cr |

📌 No further reduction notified till April 2026

💡 Practical Compliance Checklist

✔ Check turnover since FY 2017-18

✔ Verify PAN-based turnover

✔ Ensure system integration with IRP

✔ Monitor 30-day limit (for ₹10 Cr+)

✔ Train accounts team

✔ Validate IRN before issuing invoice

🎯 Key Takeaways

- ₹5 Cr threshold still applicable in 2026

- Past turnover matters (not current only)

- 30-day time limit critical for ₹10 Cr+ taxpayers

- Non-compliance = invalid invoice

- ITC risk is highest concern

The contents of this article are for general informational purposes only and are intended to provide quick access to tax rate information. Readers are advised to verify the provisions with the Income-tax Act, relevant rules, notifications, and official government sources before making financial decisions.

Visit www.cagurujiclasses.com for practical courses