The Income-tax Department has introduced Form 121 under the Income-tax Act, 2025, replacing the earlier Forms 15G & 15H. This new form simplifies the process of declaring NIL tax liability to avoid TDS deduction.

It is governed by Section 393(6) and Rule 211.

🎯 Purpose of Form 121

Form 121 is used to declare that:

👉 Your estimated total income is below taxable limit

👉 Therefore, no TDS should be deducted

👤 Eligibility

✅ Allowed:

- Resident Individuals (all age groups)

- HUFs

❌ Not Allowed:

- Companies

- Firms

- Non-residents

👉 Condition: Final tax liability must be NIL

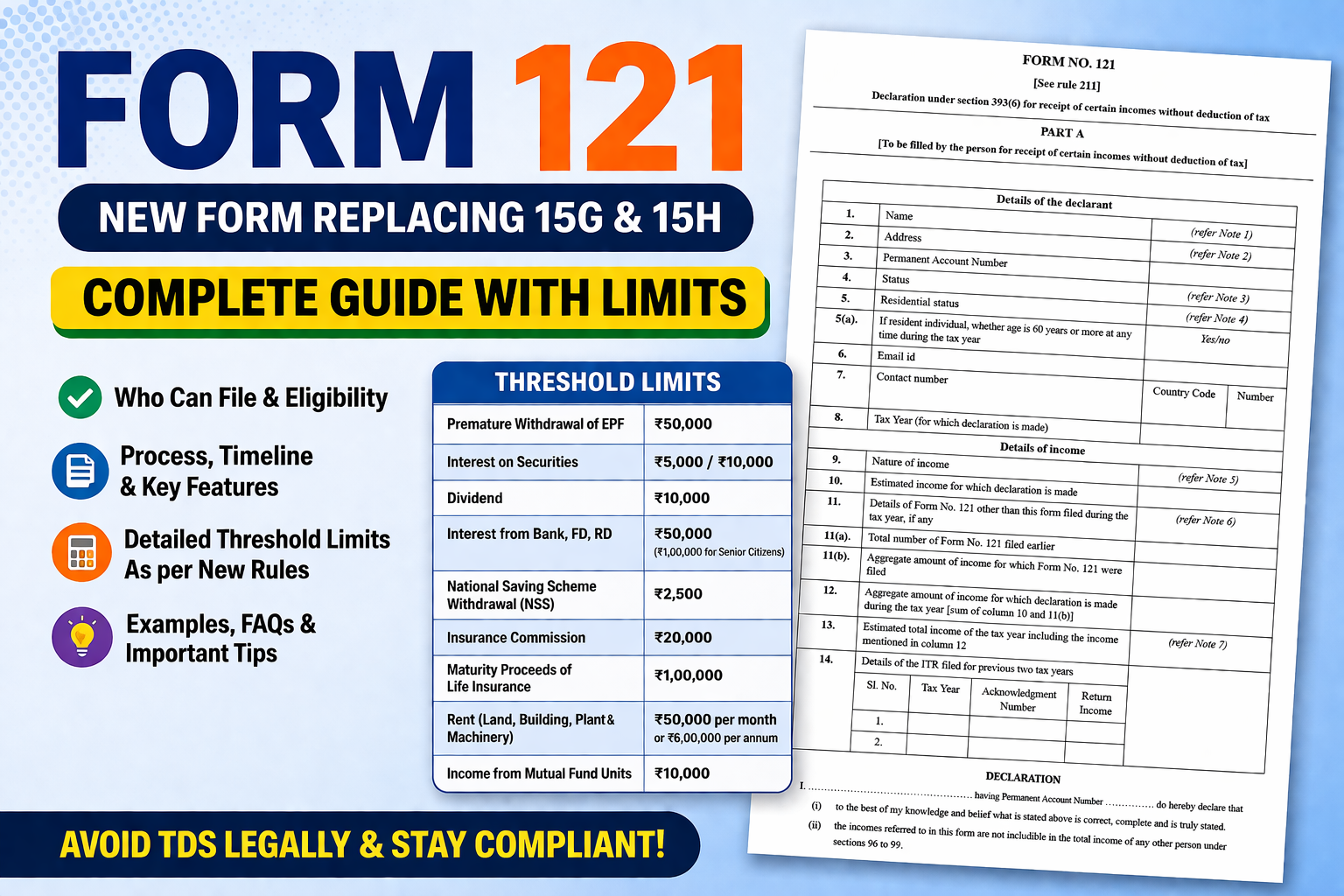

📊 Incomes for which Form 121 can be filled

Below are the important income-wise limits where Form 121 becomes relevant for avoiding TDS:

| S. No. | Nature of Payment | Threshold Limit (Financial Year) |

|---|---|---|

| 1 | Premature withdrawal of EPF | ₹50,000 |

| 2 | Interest on securities (debentures, govt. bonds, etc.) | ₹5,000 / ₹10,000 |

| 3 | Dividend income | ₹10,000 |

| 4 | Interest from Bank, FD, RD | ₹50,000 (₹1,00,000 for senior citizens) |

| 5 | National Saving Scheme (NSS) withdrawal | ₹2,500 |

| 6 | Insurance commission | ₹20,000 |

| 7 | Maturity proceeds of life insurance | ₹1,00,000 |

| 8 | Rent (land/building/plant/machinery) | ₹50,000 per month OR ₹6,00,000 annually |

| 9 | Income from mutual fund units | ₹10,000 |

👉 These limits are important triggers for TDS, and Form 121 helps avoid deduction only if tax liability is NIL.

⚠️ Important Practical Point (Very Important)

Even if your income crosses above limits:

👉 TDS applies

👉 BUT if your total income is still below taxable limit, you can submit Form 121

✔ Example:

- FD Interest = ₹60,000 (above ₹50,000 limit)

- Total income after deductions = ₹2,00,000

👉 Still eligible for Form 121 (because tax = NIL)

📋 Structure of Form 121

🧾 Part A (By Taxpayer)

- PAN, Name, DOB

- Estimated income

- Nature of income (interest, rent etc.)

- Total income estimate

- ITR filing details (last 2 years)

🏦 Part B (By Payer)

- TAN, PAN

- UIN (Unique Identification Number)

- Declaration records

📅 Filing Timing

| Activity | Timeline |

|---|---|

| Submission by taxpayer | Before income is credited |

| Monthly reporting by payer | By 7th of next month |

| TDS return reporting | Quarterly |

🔄 Process Flow

👨💼 Taxpayer:

- Check eligibility (tax NIL)

- Fill Form 121

- Submit to bank/payer

- Submit separately to each payer

🏦 Payer:

- Verify form

- Generate UIN

- Upload monthly statement

- Report in TDS return (Form 140)

🧮 Practical Examples

📌 Example 1: Bank Interest Case

Interest = ₹70,000

Deductions = ₹2,00,000

👉 Taxable income below limit

✔ Submit Form 121

✔ No TDS

📌 Example 2: Rent Case

Rent received = ₹60,000/month

👉 TDS applicable (above ₹50,000/month)

BUT

Total income after deductions = NIL

✔ Form 121 can be submitted

✔ No TDS

📌 Example 3: Wrong Declaration

Dividend = ₹2,00,000

Total taxable income = ₹8,00,000

❌ Cannot file Form 121

❌ If filed → penalty risk

⚙️ Key Features of New Form 121

- Single unified form (15G + 15H merged)

- Smart pre-filled system

- Real-time validation

- AIS integration

- UIN tracking system

❗ Important Compliance Notes

- PAN is mandatory

- Separate form for each payer

- Valid only for one financial year

- Income must still be reported in ITR

- Incorrect declaration may attract penalties