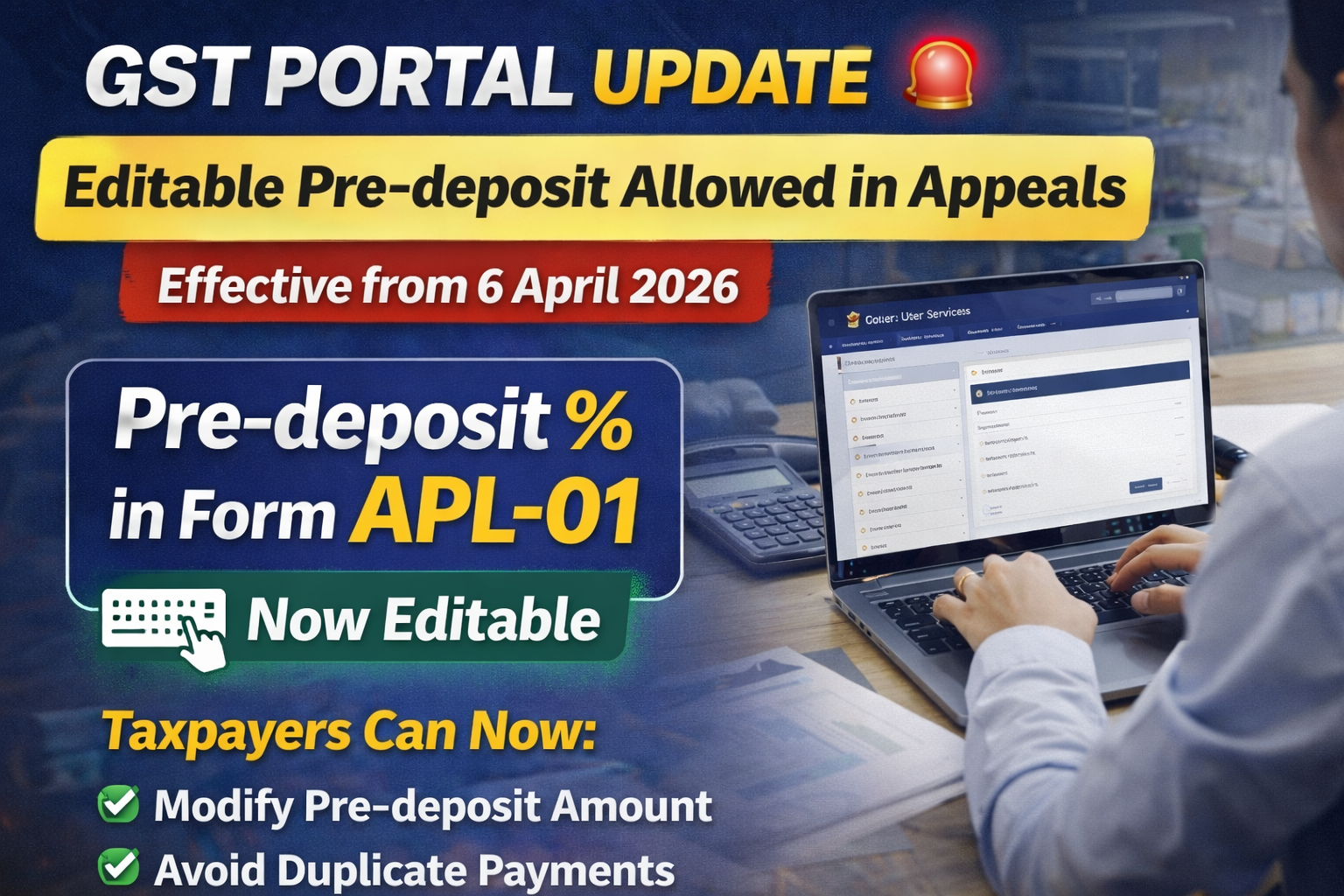

A significant and practical update has been introduced on the GST portal regarding pre-deposit while filing appealsunder GST. This change directly impacts taxpayers filing appeals in Form APL-01 and resolves long-standing practical difficulties.

🔍 Background – What is Pre-deposit under GST?

As per Section 107(6) of the CGST Act, 2017, any taxpayer filing an appeal before the Appellate Authority is required to make a mandatory pre-deposit, which includes:

- ✅ Full payment of admitted tax liability, and

- ✅ 10% of disputed tax amount (subject to maximum limits)

This pre-deposit is a pre-condition for admission of appeal.

⚠️ Issue Faced Earlier on GST Portal

Earlier, while filing Form APL-01, the GST portal:

- Auto-populated 10% pre-deposit

- ❌ Field was non-editable

This created practical challenges such as:

❗ Common Problems

- Pre-deposit already paid through DRC-03 or other mode

- Incorrect demand reflected under wrong head

- Partial payments already made but not considered

- Cases involving interest/penalty disputes only

- Situations where different interpretation of disputed amount

👉 Result: Taxpayers were forced into incorrect calculations or duplication of payments.

✅ New Update (Effective 6 April 2026)

GSTN has now introduced a major relief:

🔹 Key Change:

👉 Pre-deposit percentage field is now EDITABLE in Form APL-01

🎯 What This Means for Taxpayers

Now taxpayers can:

- ✔️ Modify pre-deposit percentage as per actual requirement

- ✔️ Adjust amount already paid

- ✔️ Avoid excess or duplicate payment

- ✔️ Ensure correct computation of disputed amount

- ✔️ Align appeal filing with actual facts of the case

🧾 Practical Scenarios Where This Helps

1. Pre-deposit Already Paid

If taxpayer already paid via DRC-03, now:

- Can reduce payable amount in APL-01

2. Incorrect Demand Classification

- If system shows higher demand → taxpayer can correct base

3. Appeal Only for Penalty/Interest

- No need to blindly apply 10% on total demand

4. Multiple Orders / Partial Appeals

- Flexibility to compute pre-deposit proportionately

⚖️ Important Safeguard

👉 This flexibility is not absolute.

- The Appellate Authority will verify:

- Correctness of pre-deposit amount

- Mode of payment

- Compliance with Section 107(6)

⚠️ Any incorrect adjustment may lead to:

- Appeal rejection

- Deficiency memo

- Additional demand

📌 Key Takeaways for Professionals

- 🔹 Always compute disputed tax correctly

- 🔹 Ensure proper documentation of earlier payments

- 🔹 Maintain reconciliation between:

- Order amount

- Paid amount

- Pre-deposit requirement

💡 Professional Tip (Important)

Before editing pre-deposit:

👉 Prepare a working sheet including:

- Total demand

- Admitted liability

- Disputed portion

- Pre-deposit calculation

- Payments already made

This avoids litigation risk at appellate stage.

🚀 Conclusion

This update is a practical and taxpayer-friendly reform by GSTN. It removes rigid system limitations and aligns portal functionality with real-life scenarios.

👉 However, with flexibility comes responsibility — accurate computation and proper justification are now more important than ever.

Visit www.cagurujiclasses.com for practical courses