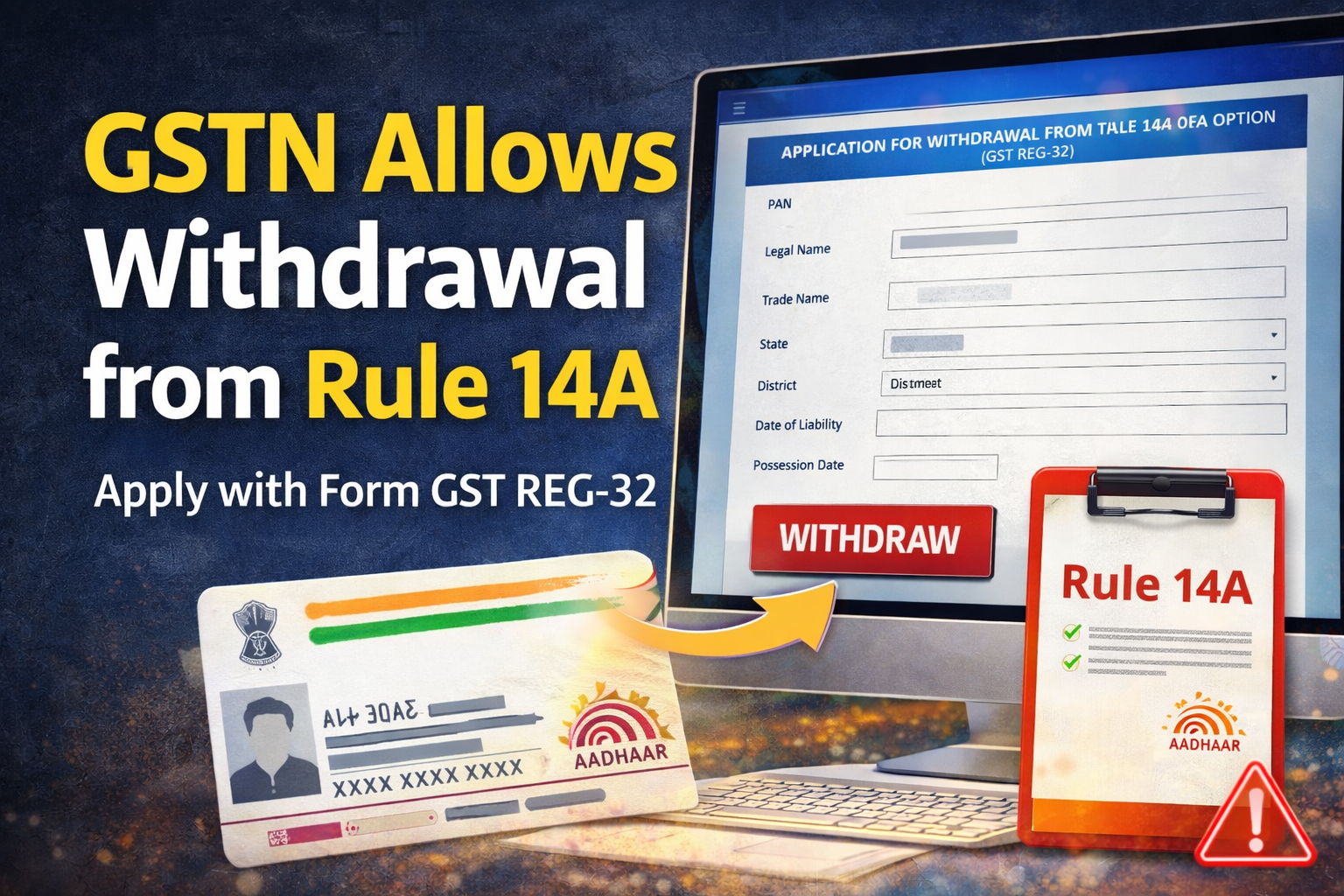

The GST ecosystem continues to evolve with new digital features aimed at improving compliance and correcting earlier procedural challenges faced by taxpayers. In line with this objective, the GST Network (GSTN) has introduced a new online facility allowing eligible taxpayers to withdraw from the registration option availed under Rule 14A of the CGST Rules.

Taxpayers can now apply for withdrawal by filing Form GST REG-32 on the GST Portal.

This new functionality addresses a practical issue faced by several businesses that opted for registration under Rule 14A but later wanted to exit the framework due to operational or compliance reasons.

Why Was This Enhancement Introduced?

Over the past few years, GST authorities have been focusing on strengthening compliance, preventing fake registrations, and ensuring accurate reporting of tax liability. Rule 14A was introduced as part of these efforts to bring certain taxpayers under a special registration and monitoring framework.

However, in practice, some taxpayers who registered under Rule 14A later found that:

- Their business model no longer required this registration option

- Compliance obligations became unnecessarily complex

- Operational changes made the registration unsuitable

Earlier, there was no streamlined mechanism to withdraw from this option once selected.

To resolve this issue and provide flexibility to taxpayers, GSTN has now enabled a structured online process through Form GST REG-32, allowing eligible taxpayers to apply for withdrawal from Rule 14A registration.

This enhancement ensures that the GST system remains flexible while still maintaining strong compliance oversight.

Who Can Apply for Withdrawal Under Rule 14A?

Only eligible active taxpayers who are currently registered under Rule 14A of the CGST Rules can apply for withdrawal.

Key eligibility conditions include:

- The taxpayer must be active on the GST portal

- Registration must have been obtained under Rule 14A

- All required GST returns must be filed before submitting the withdrawal application

Taxpayers who meet these criteria may submit the application through the GST portal.

How to Apply for Withdrawal from Rule 14A on the GST Portal

The GST portal now provides a dedicated online workflow for applying for withdrawal.

Step-by-Step Process

- Login to the GST Portal

- Navigate to the following path:

Services → Registration → Application for Withdrawal from Rule 14A

- The option will be visible only if the taxpayer is registered under Rule 14A and the GSTIN is active.

- In the application form:

- The field “Option for registration under Rule 14A” will automatically appear as “No”

- The taxpayer must provide the reason for withdrawal

- After filling the details, proceed to Aadhaar Authentication.

Aadhaar Authentication Requirement

For security and verification purposes, the withdrawal application requires Aadhaar authentication.

Authentication must be completed by:

- Primary Authorised Signatory (Mandatory)

- At least one Promoter or Partner, where applicable.

The system may require either:

- OTP-based Aadhaar authentication, or

- Biometric Aadhaar authentication, depending on risk analysis.

An Application Reference Number (ARN) will be generated only after successful Aadhaar authentication.

Key Preconditions for Filing Form GST REG-32

Before submitting the application, the taxpayer must ensure that all required GST returns are filed.

The conditions differ depending on the filing date.

If REG-32 is filed before 1 April 2026

The taxpayer must have filed:

- GST returns for at least three months

If REG-32 is filed on or after 1 April 2026

The taxpayer must have filed:

- GST returns for at least one tax period

Additional Condition

All GST returns due from:

- The effective date of registration

- Up to the date of filing REG-32

must be completely filed.

Failure to meet these conditions will prevent submission of the application.

Important Timelines for REG-32 Application

GSTN has specified strict timelines for completing the application process.

Draft Application Validity

Once the draft application is created, it must be submitted within 15 days.

Aadhaar Authentication Deadline

Aadhaar or biometric authentication must be completed within 15 days of submission.

If authentication is not completed within this time period:

- ARN will not be generated

- The application will become invalid.

Restrictions During Application Processing

Once the withdrawal application is submitted and pending approval, the taxpayer will face certain restrictions.

During this period, the taxpayer cannot file:

- Core amendment applications

- Non-core amendment applications

- Self-cancellation of GST registration

These restrictions ensure that no structural changes are made while the withdrawal application is under examination.

Post-Approval Process – Form GST REG-33

If the GST officer approves the withdrawal request, an order will be issued in Form GST REG-33.

After receiving approval, the taxpayer will be able to furnish details of output tax liability for supplies made to registered persons exceeding ₹2.5 lakh.

This reporting will be applicable from the first day of the month following the issuance of the REG-33 order.

Practical Impact for Taxpayers

The introduction of Form GST REG-32 provides several advantages:

Greater Flexibility

Taxpayers who earlier opted for Rule 14A registration now have a formal mechanism to withdraw.

Improved Compliance Management

Businesses can align their GST registration structure with their actual business operations.

Reduced Administrative Burden

A clear process avoids confusion and reduces the need for manual intervention.

Digital Transparency

The entire process is online and authenticated through Aadhaar verification.

Conclusion

The introduction of Form GST REG-32 represents another step by GSTN toward improving the flexibility and transparency of the GST system.

Taxpayers who are registered under Rule 14A but wish to withdraw from this option can now do so through a structured and fully digital process on the GST portal.

However, before applying for withdrawal, businesses must ensure that:

- All GST returns are filed

- Aadhaar authentication is completed

- The application timelines are followed carefully.

By adhering to these conditions, taxpayers can successfully exit the Rule 14A registration framework without facing compliance hurdles.

Visit www.cagurujiclasses.com for practical courses