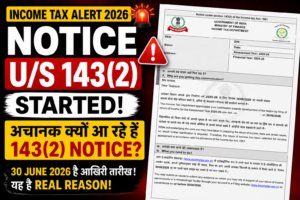

Taxpayers Across India Are Receiving 143(2) Notices – But Why Now?

Over the last few days, many taxpayers have reported receiving notices under Section 143(2) of the Income-tax Act.

As soon as taxpayers see a notice from the Income Tax Department, panic sets in. Social media is flooded with claims that lakhs of taxpayers are receiving scrutiny notices. However, the bigger question is:

If I Filed My Return Months Ago, Why Am I Receiving a Notice Now?

This is exactly what every taxpayer wants to know.

The answer lies in an important statutory deadline under the Income-tax Act which very few taxpayers are aware of.

Before you panic, let’s understand what is actually happening and whether you need to worry.

The Hidden Reason Behind the Surge in 143(2) Notices

Most taxpayers do not know that the Income Tax Department cannot issue scrutiny notices indefinitely.

For Income Tax Returns filed for AY 2025-26, the Department can issue a notice under Section 143(2) only up to:

30 June 2026

This date is extremely important.

If the Department intends to scrutinize a return filed for AY 2025-26, the notice must be issued before this deadline.

As the deadline approaches, the Department completes its risk assessment process and issues notices in selected cases.

This is the primary reason why many taxpayers are suddenly receiving scrutiny notices during June 2026.

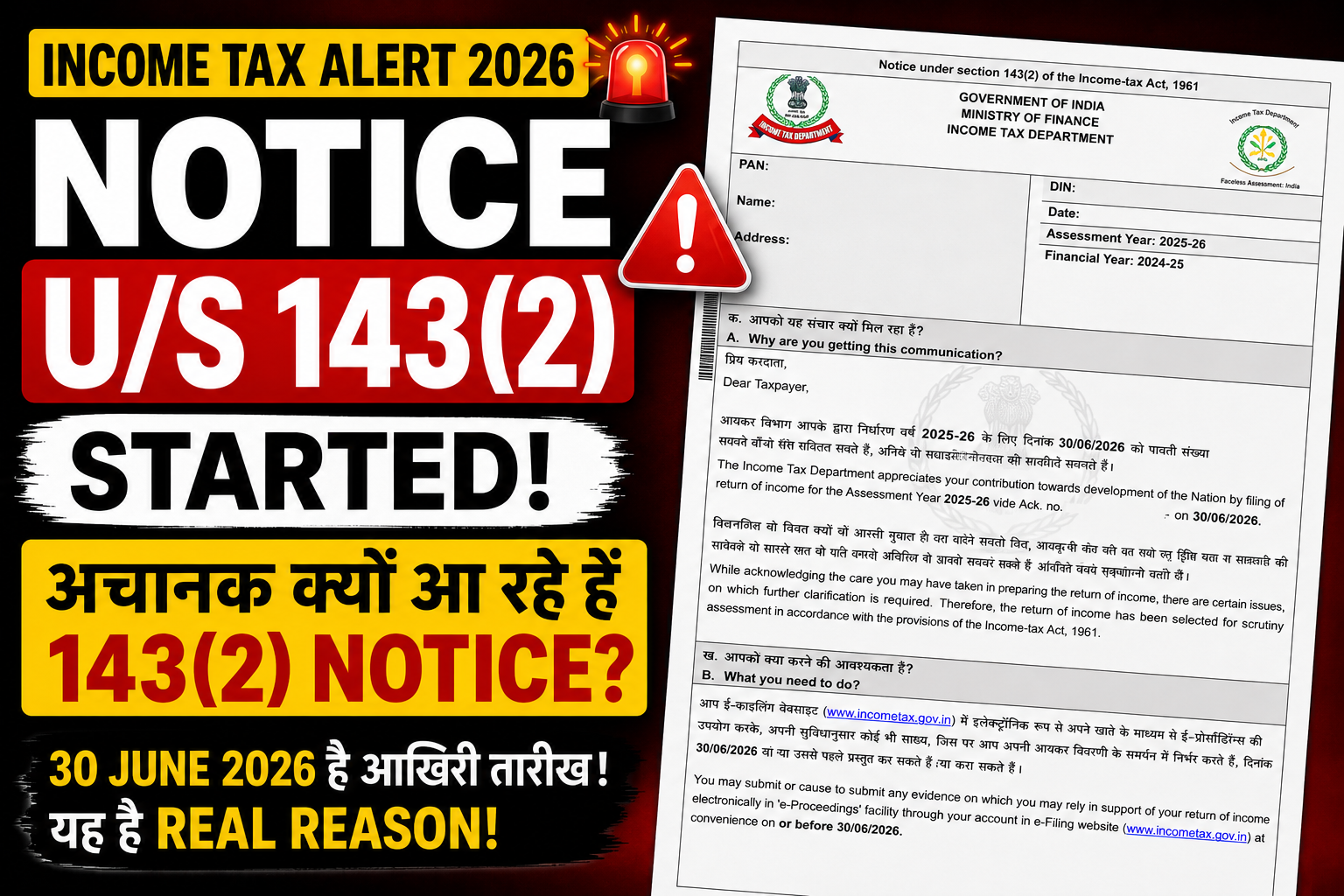

What Exactly Is Notice Under Section 143(2)?

A notice under Section 143(2) is issued when the Income Tax Department selects your Income Tax Return for detailed examination.

The objective is to verify:

- Whether income has been correctly disclosed.

- Whether deductions have been correctly claimed.

- Whether exemptions are genuine.

- Whether capital gains are properly reported.

- Whether information available with the Department matches the return filed by the taxpayer.

Receiving a scrutiny notice does not automatically mean tax evasion or concealment of income.

It simply means the Department wants additional verification.

Why Was Your Return Selected for Scrutiny?

Many taxpayers assume that once the return is processed, everything is over.

However, the Income Tax Department now uses advanced data analytics and artificial intelligence tools to identify high-risk cases.

The Department compares information from multiple databases before selecting cases for scrutiny.

Top Reasons Why Taxpayers May Receive Notice U/S 143(2)

1. AIS and ITR Mismatch

One of the biggest reasons for scrutiny today is mismatch between:

- Annual Information Statement (AIS)

- Form 26AS

- Income Tax Return

Even a small mismatch can attract departmental attention.

2. High-Value Transactions

The Department receives information regarding:

- Large bank deposits

- Property transactions

- High-value investments

- Credit card spending

- Foreign remittances

If such transactions appear disproportionate to reported income, scrutiny may follow.

3. Sale of Property and Capital Gains

Taxpayers who have sold:

- Land

- House property

- Commercial property

- Shares

- Mutual funds

may be selected if capital gains are not correctly reported.

4. Large Refund Claims and Fake Deductions or Exemptions

Cases involving substantial tax refunds are often subjected to additional verification before final acceptance.

5. Business Losses and Unusual Deductions

Returns showing:

- Large business losses

- Significant deductions

- Unusually low profits

may attract scrutiny.

6. Foreign Assets and Foreign Income

The Department has significantly increased monitoring of:

- Overseas investments

- Foreign bank accounts

- Foreign income

- International transactions

Failure to report such information accurately can result in scrutiny proceedings.

Does Receiving a 143(2) Notice Mean You Have Done Something Wrong?

Absolutely not.

This is one of the biggest misconceptions among taxpayers.

A scrutiny notice merely means that the Department wants to verify certain information.

In fact, many genuine taxpayers receive scrutiny notices every year and successfully complete proceedings after submitting supporting documents.

Therefore, receiving a notice should not be viewed as proof of any wrongdoing.

What Happens After Receiving Notice U/S 143(2)?

The scrutiny process is generally conducted online through the faceless assessment system.

The taxpayer is required to:

Step 1

Login to the Income Tax Portal.

Step 2

Check the notice and accompanying questionnaire.

Step 3

Collect supporting documents.

Step 4

Submit explanations through e-Proceedings.

Step 5

Respond within the prescribed timeline.

All communications generally take place electronically.

What Documents May Be Asked During Scrutiny?

Depending upon the nature of the case, the Department may ask for:

- Bank statements

- Property purchase documents

- Property sale deeds

- Capital gain calculations

- Books of accounts

- GST records

- Loan confirmations

- Investment proofs

- Foreign asset disclosures

- Income supporting documents

The exact requirements vary from case to case.

Can You Ignore a 143(2) Notice?

The answer is NO.

Ignoring a notice can lead to:

- Best Judgment Assessment

- Addition of income

- Tax demand

- Interest liability

- Penalty proceedings

Therefore, every notice should be reviewed carefully and responded to on time.

Important Date Every Taxpayer Should Remember

| Particulars | Details |

|---|---|

| Financial Year | 2024-25 |

| Assessment Year | 2025-26 |

| Last Date for Issue of Notice U/S 143(2) | 30 June 2026 |

This deadline explains why taxpayers are suddenly witnessing a sharp increase in scrutiny notices during June 2026.

The Biggest Takeaway

If you have received a notice under Section 143(2), do not panic.

The notice does not mean that you have committed tax evasion.

The real reason behind the sudden increase in notices is the statutory deadline of 30 June 2026 for AY 2025-26 scrutiny selection.

Read the notice carefully, gather supporting documents, and submit a proper response within the prescribed time.

Timely compliance and proper documentation are the keys to successfully handling scrutiny proceedings.

Frequently Asked Questions (FAQs)

Is receiving a notice under Section 143(2) serious?

Yes, it should be taken seriously, but it does not automatically imply any wrongdoing.

Why are so many taxpayers receiving notices in June 2026?

Because 30 June 2026 is the last date for issuing scrutiny notices for AY 2025-26.

Can scrutiny be conducted online?

Yes. Most scrutiny proceedings are conducted through the faceless assessment mechanism.

Can a Chartered Accountant represent me?

Yes. An authorized Chartered Accountant can assist and represent the taxpayer during scrutiny proceedings.

What should I do immediately after receiving the notice?

Login to the Income Tax Portal, review the notice carefully, collect supporting documents, and submit a timely response.