One of the most common questions faced by business owners, professionals, tax practitioners and CA students is whether Tax Audit is applicable in a particular case.

At first glance, the answer appears simple. Many taxpayers believe that if turnover exceeds ₹1 crore, Tax Audit becomes mandatory. Others are aware of the enhanced limit of ₹10 crore and conclude that Tax Audit is not required unless turnover crosses that threshold. Some taxpayers rely upon presumptive taxation schemes under Sections 44AD or 44ADA and assume that Tax Audit provisions can always be avoided.

Unfortunately, the law is not as straightforward as it appears.

The applicability of Tax Audit under Section 44AB depends upon multiple factors including the nature of activity carried on by the assessee, turnover or gross receipts, percentage of cash transactions, eligibility for presumptive taxation schemes and the amount of income declared by the taxpayer.

As a result, two businesses having the same turnover may have completely different Tax Audit obligations. Similarly, a professional earning ₹60 lakh may be subject to a different set of provisions than a business owner having turnover of several crores.

The confusion has increased further after the introduction of enhanced turnover limits of ₹10 crore for businesses and increased presumptive taxation thresholds of ₹3 crore under Section 44AD and ₹75 lakh under Section 44ADA. Many taxpayers incorrectly assume that these limits are interchangeable, whereas each provision serves an entirely different purpose.

In this article, we will examine the provisions relating to Tax Audit under Section 44AB in a practical and comprehensive manner. We will discuss the audit requirements applicable to businesses and professionals, understand the impact of presumptive taxation schemes under Sections 44AD, 44ADA and 44AE, analyse the enhanced turnover limits available in cases involving digital transactions and review practical examples to determine when Tax Audit becomes mandatory.

By the end of this article, you will be able to determine the applicability of Tax Audit in almost every practical situation without confusion.

Understanding the Purpose of Tax Audit

Tax Audit under Section 44AB is not merely a procedural requirement. The objective of Tax Audit is to ensure that taxpayers maintain proper books of account, correctly compute taxable income and comply with the provisions of the Income-tax Act.

Through the audit process, the Chartered Accountant examines the books of account and reports various particulars to the Income Tax Department in the prescribed audit report.

The audit helps improve tax compliance, reduces reporting errors and provides greater transparency in financial reporting.

However, Tax Audit is not applicable to every taxpayer. The law prescribes specific thresholds and conditions that determine whether an audit is required.

Therefore, before examining the turnover limits, it is important to understand that the applicability of Tax Audit depends primarily upon the category in which the taxpayer falls.

Classification of Cases for Tax Audit Purposes

For practical purposes, Tax Audit cases can be divided into five broad categories:

| Category | Relevant Provision |

|---|---|

| Business – Normal Provisions | Section 44AB |

| Profession – Normal Provisions | Section 44AB |

| Presumptive Business | Section 44AD |

| Presumptive Profession | Section 44ADA |

| Goods Carriage Business | Section 44AE |

The first step in determining Tax Audit applicability is always to identify the correct category. Once the category is identified, the relevant turnover limits and conditions can be applied.

Tax Audit in Case of Business

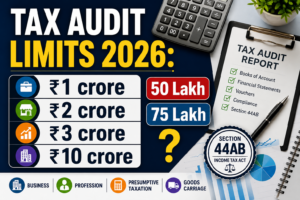

For persons carrying on business, Section 44AB provides that Tax Audit becomes mandatory where total sales, turnover or gross receipts exceed the prescribed threshold during the previous year.

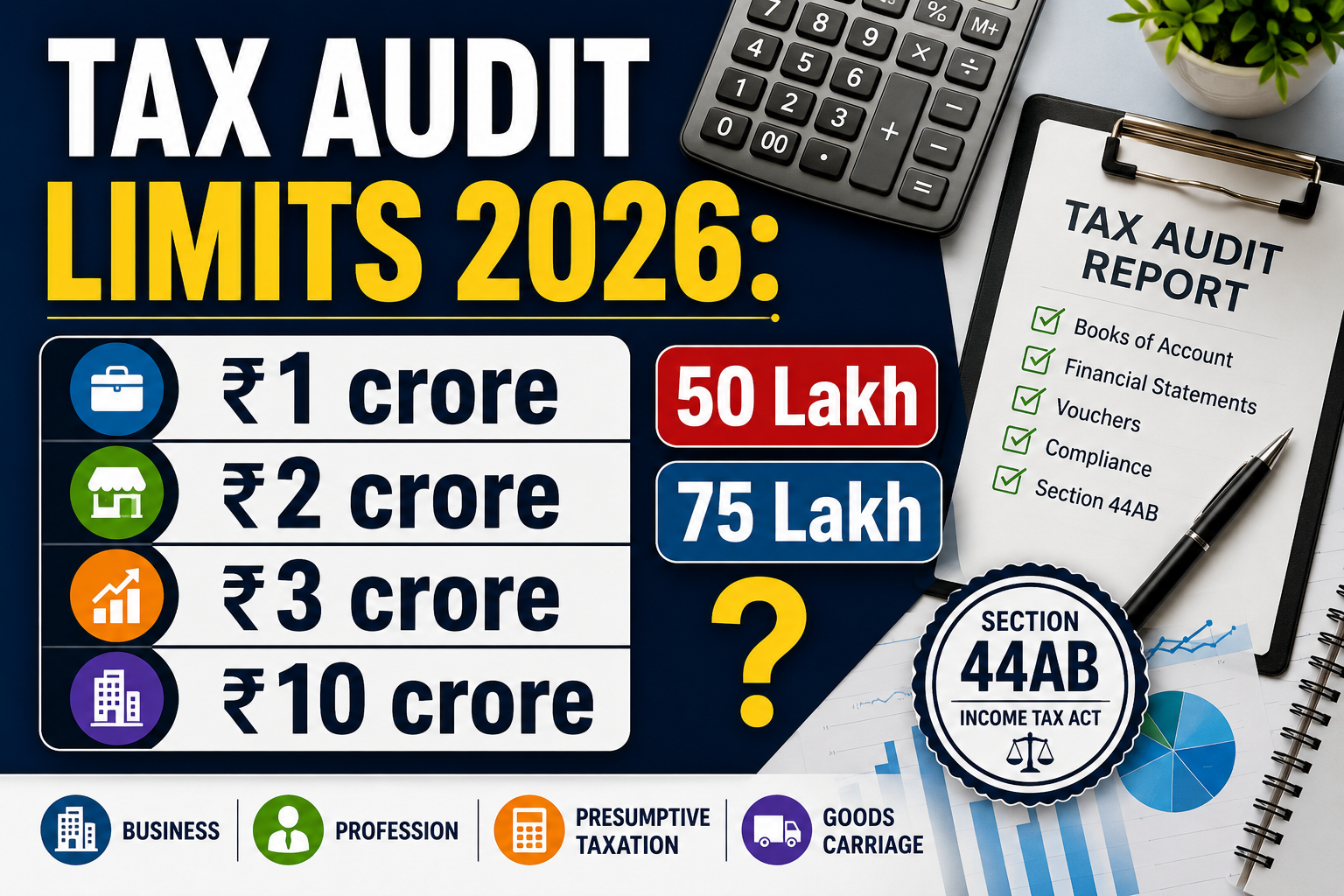

Traditionally, the threshold for business assessees has been ₹1 crore.

Accordingly, where turnover exceeds ₹1 crore, Tax Audit becomes applicable.

However, in order to encourage digital transactions and reduce cash-based dealings, the Government introduced a significant relaxation by increasing the threshold from ₹1 crore to ₹10 crore in specified cases.

This relaxation is available only where:

- Aggregate cash receipts do not exceed 5% of total receipts; and

- Aggregate cash payments do not exceed 5% of total payments.

Both conditions must be satisfied simultaneously.

If either condition is violated, the enhanced threshold is not available and the taxpayer must revert to the normal threshold of ₹1 crore.

Example

Suppose a trader has turnover of ₹6 crore during FY 2025-26.

Cash receipts constitute only 2% of total receipts and cash payments constitute 3% of total payments.

Since both percentages are within the prescribed limit of 5%, the taxpayer becomes eligible for the enhanced threshold of ₹10 crore.

As turnover of ₹6 crore does not exceed ₹10 crore, Tax Audit will not be applicable.

On the other hand, if cash payments increase to 8% of total payments, the enhanced threshold becomes unavailable.

The applicable threshold will revert to ₹1 crore and since turnover exceeds ₹1 crore, Tax Audit will become mandatory.

Presumptive Taxation Scheme for Business – Section 44AD

Section 44AD is one of the most beneficial provisions available to small businesses. The primary objective of this scheme is to reduce the compliance burden on eligible taxpayers by relieving them from the requirement of maintaining detailed books of account and getting those books audited in specified circumstances.

However, Section 44AD is often misunderstood. Many taxpayers believe that once they opt for Section 44AD, Tax Audit provisions cease to apply permanently. This is not correct. The applicability of Tax Audit under presumptive taxation provisions depends upon multiple factors and therefore requires careful analysis.

Section 44AD is available only to Resident Individuals, Resident Hindu Undivided Families (HUFs) and Resident Partnership Firms. Limited Liability Partnerships (LLPs) are specifically excluded from this scheme. Further, businesses earning income by way of commission, brokerage, agency business or certain specified activities are not eligible to opt for Section 44AD.

Before discussing Tax Audit implications, it is important to understand the turnover limits prescribed under this scheme.

Under normal circumstances, Section 44AD can be opted if the turnover or gross receipts of the business do not exceed ₹2 crore during the previous year. However, in order to encourage digital transactions, the Government has introduced an enhanced threshold of ₹3 crore. This enhanced limit becomes available where cash receipts during the year do not exceed 5% of the total turnover or gross receipts.

The distinction between the ₹3 crore limit under Section 44AD and the ₹10 crore limit under Section 44AB is extremely important. The ₹3 crore threshold determines eligibility to opt for presumptive taxation, whereas the ₹10 crore threshold determines whether Tax Audit is applicable in certain business cases. These two limits serve entirely different purposes and should never be confused with each other.

Example

Suppose Mr. Aman is engaged in a trading business and his turnover during FY 2025-26 amounts to ₹2.75 crore.

If cash receipts constitute only 2% of total turnover, he becomes eligible for the enhanced threshold of ₹3 crore and can opt for Section 44AD.

However, if cash receipts constitute 12% of turnover, the enhanced threshold will not be available. In such a situation, the normal threshold of ₹2 crore will apply and Mr. Aman will not be eligible to opt for Section 44AD.

Presumptive Income Under Section 44AD

Where Section 44AD is opted, income is presumed to be:

| Nature of Receipts | Presumptive Income |

|---|---|

| Digital Receipts | 6% of turnover |

| Cash Receipts | 8% of turnover |

Taxpayers are free to declare higher income if their actual profit exceeds these percentages.

The complexity arises when the taxpayer wishes to declare income lower than the prescribed presumptive rates.

Under Section 44AD(4) and Section 44AD(5), where a taxpayer who has opted for presumptive taxation fails to comply with the prescribed conditions and declares lower income than the presumptive income, maintenance of books of account and Tax Audit requirements may arise, particularly where the total income exceeds the basic exemption limit.

Accordingly, taxpayers should not assume that merely opting for Section 44AD permanently eliminates the possibility of Tax Audit. The provisions relating to lower income declaration and lock-in requirements must always be examined.

Presumptive Taxation Scheme for Professionals – Section 44ADA

Recognising that many professionals face compliance challenges similar to small businesses, the Income-tax Act provides a separate presumptive taxation scheme for professionals under Section 44ADA.

This scheme is available only to Resident Individuals and Resident Partnership Firms carrying on specified professions. LLPs are not eligible for this scheme.

The professions generally covered include legal, medical, engineering, architectural, accountancy, technical consultancy and other notified professions.

Under the normal provisions, Tax Audit becomes mandatory for professionals when gross receipts exceed ₹50 lakh. However, Section 44ADA provides an alternative mechanism for eligible professionals.

The threshold for opting into Section 44ADA is ₹50 lakh under normal circumstances. Similar to Section 44AD, an enhanced threshold of ₹75 lakh is available where cash receipts do not exceed 5% of total receipts.

This enhancement has significantly expanded the scope of presumptive taxation for professionals.

Example

Consider a Chartered Accountant having gross professional receipts of ₹70 lakh during FY 2025-26.

If cash receipts constitute only 3% of total receipts, the enhanced threshold of ₹75 lakh becomes available and the professional may opt for Section 44ADA.

However, if cash receipts exceed 5%, the enhanced threshold will not be available and eligibility must be examined with reference to the normal threshold of ₹50 lakh.

Presumptive Income Under Section 44ADA

Under this scheme, income is deemed to be 50% of gross receipts.

For example, if a professional earns gross receipts of ₹60 lakh, presumptive income will ordinarily be ₹30 lakh.

The law assumes that the remaining 50% represents expenses incurred for earning the professional income.

However, situations often arise where a professional believes that actual income is lower than 50% of gross receipts.

In such cases, the professional may declare lower income. However, if total income exceeds the basic exemption limit, books of account may have to be maintained and Tax Audit requirements may become applicable.

Therefore, professionals intending to declare income below the presumptive rate should carefully evaluate the compliance consequences before doing so.

Goods Carriage Business – Section 44AE

Section 44AE provides a separate presumptive taxation scheme for taxpayers engaged in the business of plying, hiring or leasing goods carriages.

This provision recognises the practical difficulties involved in maintaining detailed books of account for small transport operators.

The scheme is available only where the taxpayer owns not more than ten goods vehicles at any time during the previous year.

Unlike Sections 44AD and 44ADA, Section 44AE prescribes vehicle-based presumptive income rather than a percentage of turnover.

Computation of Presumptive Income

| Type of Vehicle | Presumptive Income |

|---|---|

| Heavy Goods Vehicle | ₹1,000 per ton of gross vehicle weight or unladen weight per month or part thereof |

| Other Goods Vehicle | ₹7,500 per vehicle per month or part thereof |

Example

Suppose a transporter owns five goods vehicles other than heavy goods vehicles throughout the financial year.

Presumptive income under Section 44AE would be:

₹7,500 × 5 Vehicles × 12 Months

= ₹4,50,000

If the taxpayer accepts the presumptive income computed under Section 44AE, the compliance burden remains relatively low.

However, where lower income is claimed and the taxpayer seeks to depart from the presumptive provisions, maintenance of books of account and Tax Audit implications may need to be examined.

Comparative Analysis of Sections 44AB, 44AD, 44ADA and 44AE

The following table provides a quick comparison of the major provisions:

| Particulars | Section 44AB Business | Section 44AD | Section 44ADA | Section 44AE |

|---|---|---|---|---|

| Applicable To | Business | Eligible Small Business | Eligible Professionals | Goods Carriage Business |

| Basic Threshold | ₹1 Crore | ₹2 Crore | ₹50 Lakh | Not Based on Turnover |

| Enhanced Threshold | ₹10 Crore | ₹3 Crore | ₹75 Lakh | Not Applicable |

| Digital Transaction Condition | Yes | Yes | Yes | No |

| Presumptive Income | Not Applicable | 6% / 8% | 50% | Fixed Amount Per Vehicle |

| LLP Eligible | Yes | No | No | Yes |

| Tax Audit Applicability | Based on turnover | if income is less that 6/8% | if income is less that 50% | if income is less fixed limits |

Common Mistakes Made While Determining Tax Audit Applicability

One of the most common mistakes is confusing the ₹3 crore limit under Section 44AD with the ₹10 crore threshold applicable for Tax Audit purposes under Section 44AB.

Another frequent error is assuming that all professionals enjoy the benefit of the ₹10 crore threshold. This benefit is available only in specified business cases and does not apply to professionals.

Taxpayers also frequently assume that once Section 44AD or Section 44ADA is opted, Tax Audit can never become applicable. This belief is incorrect because lower income declarations and specific statutory conditions may still trigger audit requirements.

Many taxpayers also ignore the importance of the 5% cash transaction condition while determining eligibility for enhanced thresholds.

Such mistakes often result in non-compliance and may lead to penalties.

Practical Framework for Determining Tax Audit Applicability

Whenever a Tax Audit question arises, the following sequential approach should be adopted:

- Identify whether the activity constitutes a business or profession.

- Determine whether presumptive taxation provisions are applicable.

- Verify turnover or gross receipts.

- Examine cash receipt and cash payment percentages.

- Check whether enhanced thresholds are available.

- Determine whether income is being declared below the presumptive rates.

- Examine whether total income exceeds the applicable exemption limit.

- Apply the relevant provisions of Section 44AB.

Following this systematic framework ensures that Tax Audit applicability can be determined accurately in almost every practical case.

Frequently Asked Questions (FAQs)

Is Tax Audit applicable if business turnover is ₹5 crore?

It depends. If cash receipts and cash payments do not exceed 5% of total receipts and payments respectively, the enhanced threshold of ₹10 crore may apply and Tax Audit may not be required.

Can a professional avail the ₹10 crore threshold?

No. The enhanced threshold of ₹10 crore is available only in specified business cases.

What is the turnover limit under Section 44AD?

The normal limit is ₹2 crore. It may increase to ₹3 crore where cash receipts do not exceed 5% of total receipts.

What is the gross receipt limit under Section 44ADA?

The normal threshold is ₹50 lakh. It may increase to ₹75 lakh where cash receipts do not exceed 5% of total receipts.

Is LLP eligible for Section 44AD or Section 44ADA?

No. LLPs are specifically excluded from these presumptive taxation schemes.

Does declaring lower income automatically trigger Tax Audit?

Not always. Additional statutory conditions must also be examined before concluding that Tax Audit is applicable.

Conclusion

The applicability of Tax Audit cannot be determined merely by looking at turnover figures. A correct conclusion requires examination of the nature of activity, eligibility for presumptive taxation, turnover or receipt thresholds, percentage of cash transactions and the income actually declared by the taxpayer.

The introduction of enhanced thresholds of ₹10 crore for businesses, ₹3 crore under Section 44AD and ₹75 lakh under Section 44ADA has certainly reduced compliance requirements for many taxpayers. However, these provisions have also increased the possibility of confusion because each threshold serves a different purpose.

Therefore, before concluding whether Tax Audit is applicable, taxpayers and professionals should adopt a structured approach by first identifying the relevant provision and then applying the corresponding conditions. Once this methodology is followed, even complex Tax Audit situations become much easier to analyse and resolve.

Visit www.cagurujiclasses.com for practical courses