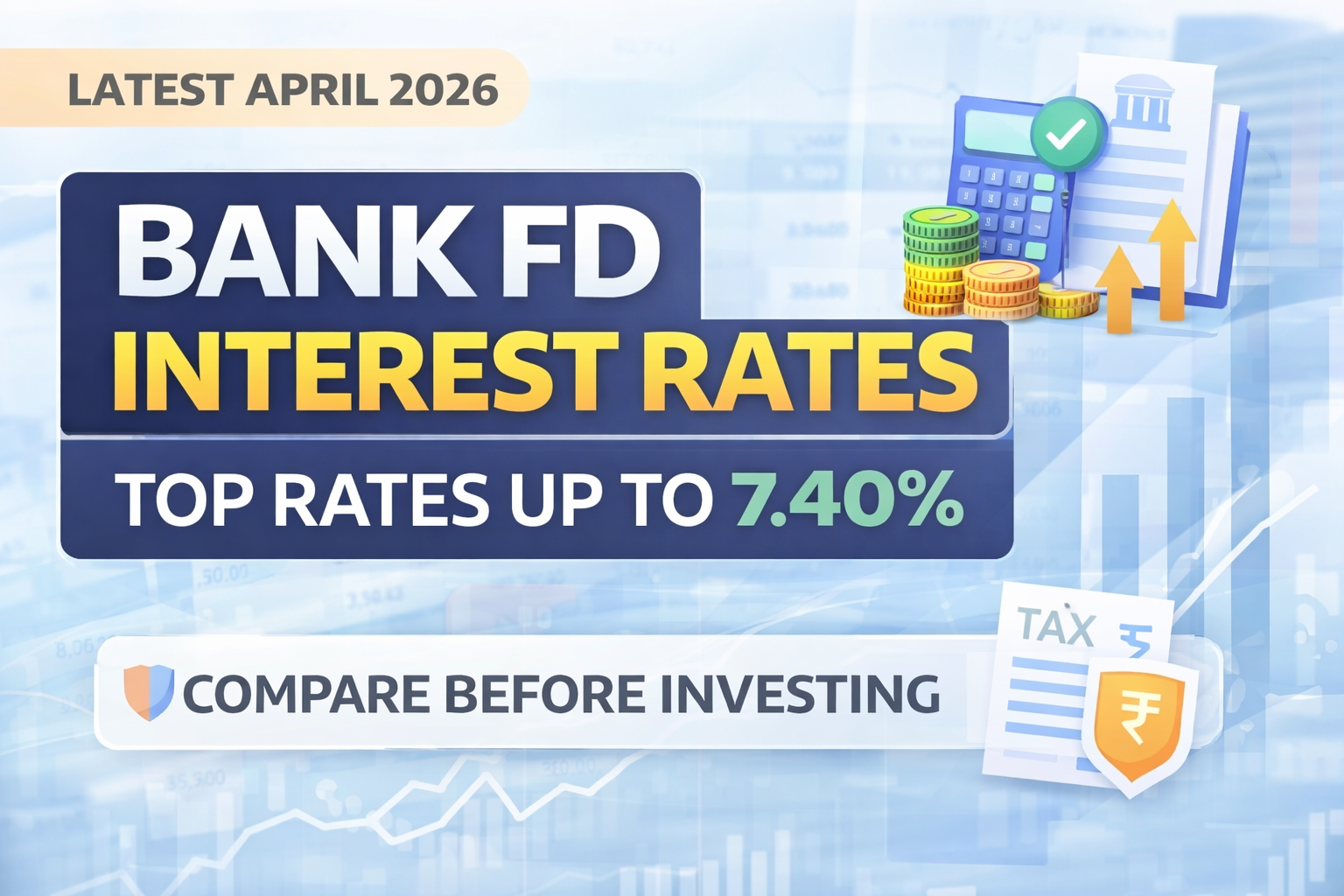

With changing economic conditions and RBI policy impact, Fixed Deposit (FD) interest rates have seen notable variations across banks. As of April 2026, private sector banks are offering competitive rates, making it important for investors to compare before investing.

This article provides a detailed analysis of latest FD interest rates, helping you choose the best option based on tenure and returns.

Photo Credit money control

💰 Overview of FD Interest Rates – April 2026

- Interest rates range between ~5.00% to 7.40% p.a.

- Higher rates are generally offered for mid-term tenures (1–3 years)

- Some small private banks are offering above 7% returns

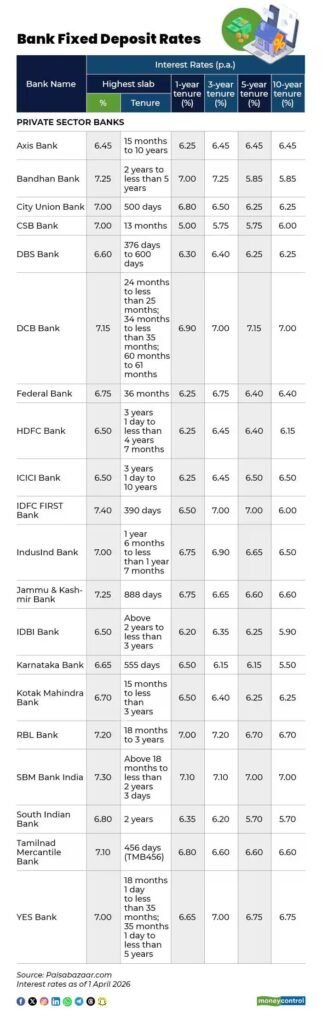

🏦 Top Banks Offering Highest FD Rates

🔝 1. IDFC FIRST Bank – Up to 7.40%

- Tenure: ~390 days

- Among the highest FD rates currently available

🔝 2. Bandhan Bank – Up to 7.25%

- Best for 2–5 year tenure

🔝 3. Jammu & Kashmir Bank – Up to 7.25%

- Competitive rates for mid-term investments

🔝 4. RBL Bank – Up to 7.20%

- Strong returns in 18 months to 3 years

🔝 5. DCB Bank – Up to 7.15%

- Good for diversified tenure options

📉 Moderate FD Rate Banks (6.5% – 7%)

These banks offer stable and reliable returns:

- HDFC Bank – ~6.50%

- ICICI Bank – ~6.50%

- Axis Bank – ~6.45%

- Kotak Mahindra Bank – ~6.70%

- Federal Bank – ~6.75%

👉 Suitable for low-risk investors prioritizing safety + brand trust

📊 Low to Mid Range FD Rates

- CSB Bank – starts around 5.00% (short tenure)

- South Indian Bank – ~5.70% to 6.80%

- Karnataka Bank – ~5.50% to 6.65%

👉 Better suited for short-term parking of funds

⏳ Tenure-wise Insights

📌 1-Year FD

- Range: ~6.25% to 7.00%

- Best: Bandhan Bank, RBL Bank

📌 3-Year FD

- Range: ~6.40% to 7.25%

- Best: IDFC FIRST Bank, YES Bank

📌 5-Year FD

- Range: ~5.70% to 7.00%

- Lock-in important (especially for tax-saving FD)

📌 10-Year FD

- Range: ~5.85% to 7.00%

- Suitable for long-term conservative investors

⚖️ Important Factors Before Choosing FD

✅ 1. Interest Rate vs Safety

- Higher rate often = smaller bank

- Balance between return & credibility

✅ 2. Tenure Selection

- Mid-term (1–3 years) currently gives best returns

✅ 3. Liquidity Needs

- Premature withdrawal penalty applicable

✅ 4. Taxation

- FD interest is fully taxable under Income Tax

- TDS applicable as per provisions

💡 Taxation on FD Interest

- Interest is taxable under “Income from Other Sources”

- TDS applicable if interest exceeds threshold

- Senior citizens get higher exemption limits

👉 Suggestion: Consider Form 121 (if eligible)

🔥 Expert Insight

- Current trend shows peak or near-peak interest rates

- Locking funds for 2–3 years can be beneficial

- Avoid long-term lock-in unless rates are very attractive

FD remains one of the safest investment options, especially for conservative investors. However, in April 2026, rate comparison is crucial as differences between banks can significantly impact returns.

Investors should take a balanced decision considering interest rate, tenure, and tax implications before investing.

📢 Disclaimer

Interest rates are subject to change. Investors should verify latest rates from respective bank websites before investing.

Visit www.cagurujiclasses.com for practical courses