For the Financial Year 2025–26, the Income Tax Returns will be filed in 2026 as per the applicable due dates. The government has already notified the new ITR forms for Assessment Year 2026–27, introducing several important changes aimed at improving transparency, compliance, and reporting accuracy.

In this article, we have covered all the key changes applicable to ITR-1, ITR-2, ITR-3 and ITR-4 in a simplified manner.

ITR-1 (Sahaj)

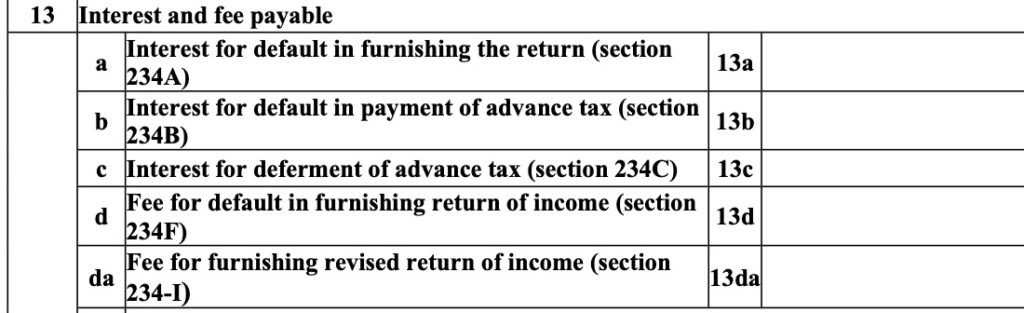

- A new reporting requirement has been introduced to disclose fee paid under section 234I for filing a revised return. This comes after extension of the revised return timeline to 12 months.

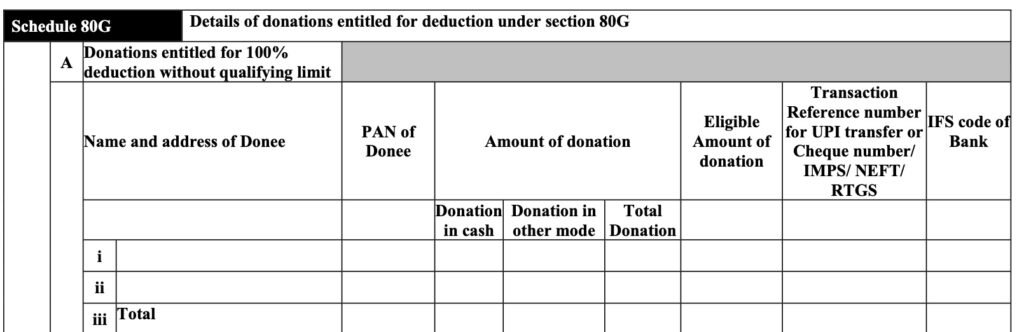

- In Section 80G (Donations), taxpayers are now required to furnish:

- IFSC Code of the bank

- Transaction reference number (UPI/NEFT/RTGS/Cheque etc.)

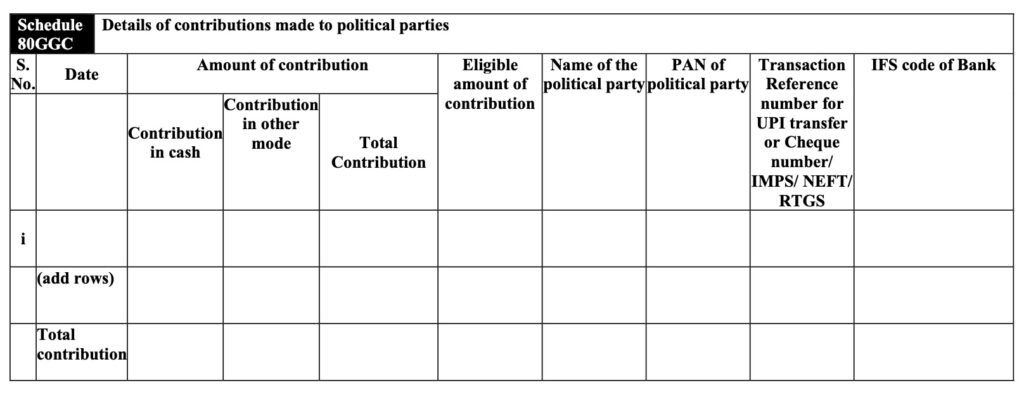

- In Section 80GGC (Political Donations), additional disclosures are mandatory:

- Name of the political party

- PAN of the political party

- Major relaxation introduced:

Taxpayers can now report up to 2 house properties. Earlier, only 1 house property was allowed in ITR-1.

- Fields relating to foreign retirement accounts have been removed, aligning with eligibility conditions of ITR-1.

- Details of representative assessee have been simplified. Now only:

- Name

- Email ID

- Contact number

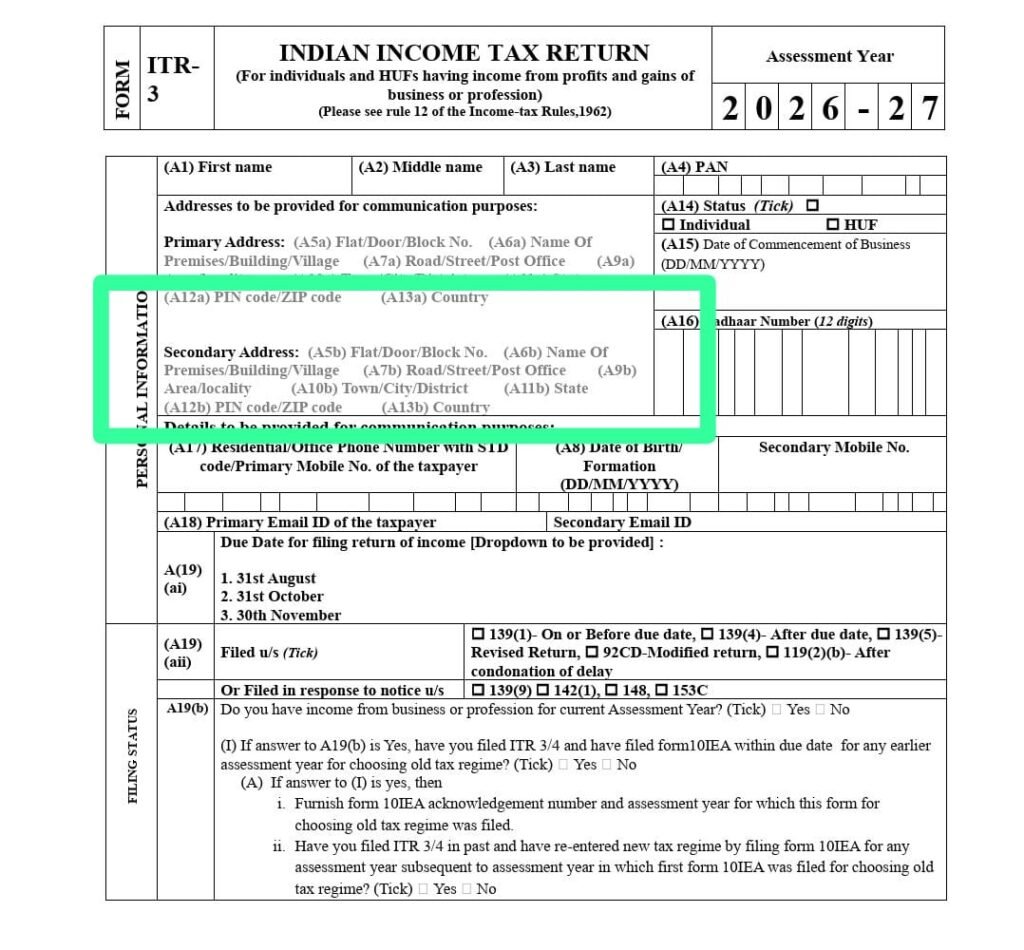

- A new concept of secondary address has been introduced along with primary and secondary contact details.

🔹 ITR-2

- Reporting of fee under section 234I for revised return has been added.

- Additional compliance in Section 80G & 80GGC:

- Mandatory reporting of IFSC and transaction reference number

- Political party name and PAN required

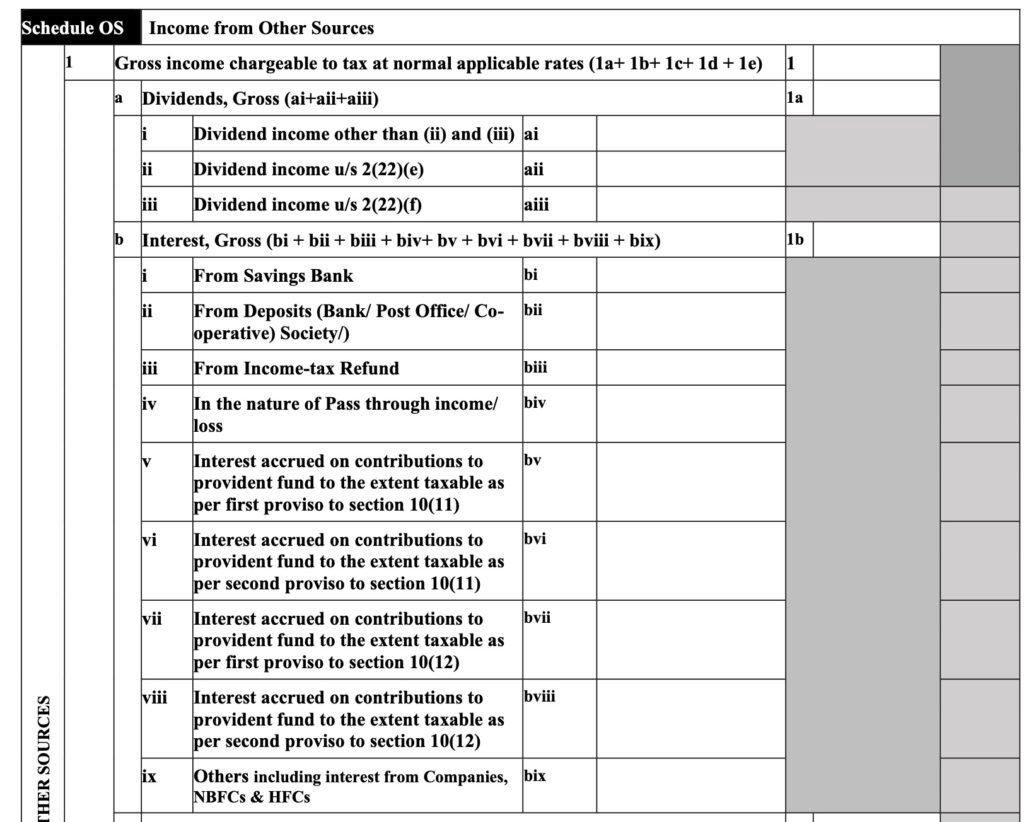

- In Schedule OS, specific clarification introduced:

- Interest income from companies, NBFCs and HFCs must be reported under “Other” category.

- Capital gain reporting simplified:

- No requirement to bifurcate gains before and after 23 July 2024.

- A new reporting requirement added for interest taxable at concessional rate of 9% (section 194LC).

- Simplification in representative assessee details and introduction of secondary address similar to ITR-1.

🔹 ITR-3 (Business/Profession)

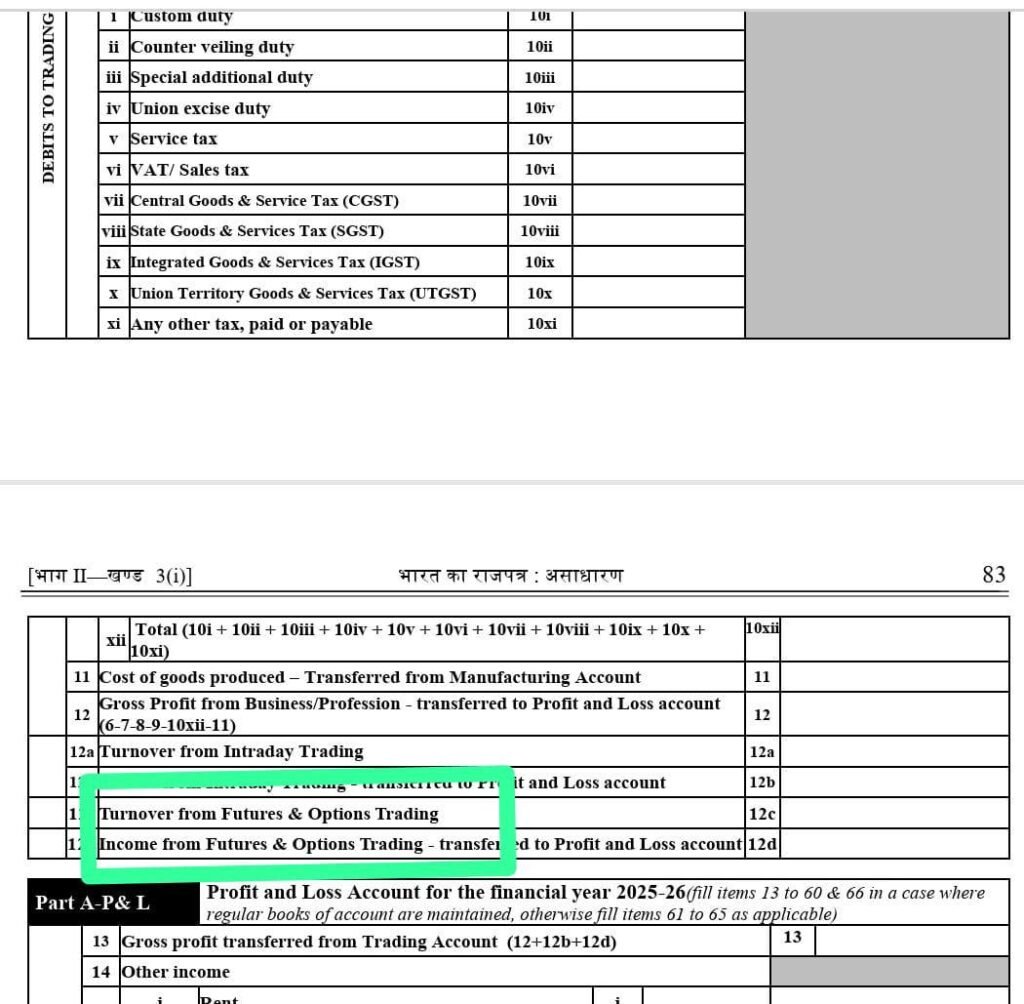

- New disclosure for Futures & Options (F&O):

- Turnover from F&O

- Income from F&O

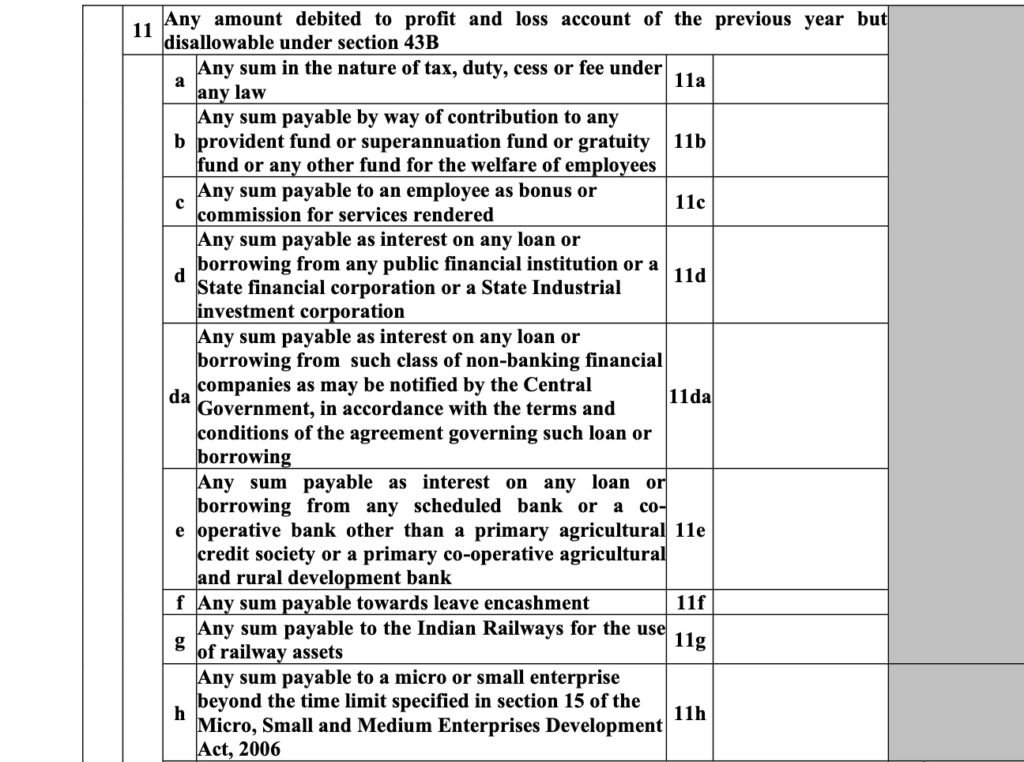

- A new reporting requirement added for MSME interest disallowance under section 43B(h).

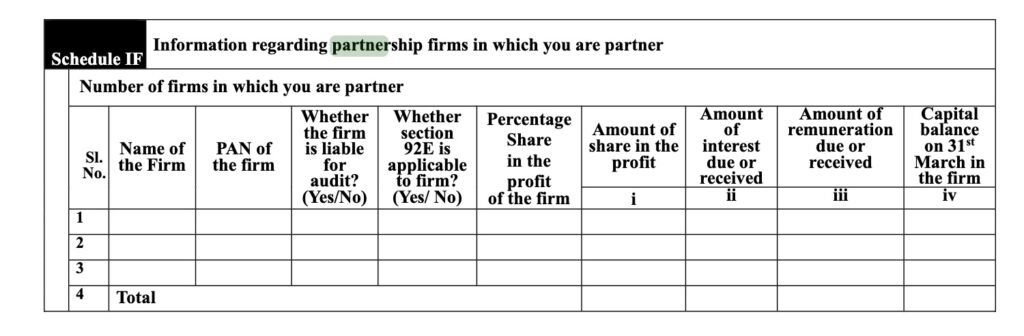

- In Schedule IF (Partnership firms):

- Interest received/due must be disclosed

- Remuneration received/due must be disclosed

- Reporting of fee under section 234I introduced.

- Changes in Section 80G & 80GGC similar to other ITR forms.

- Due date updated in the form:

- 31 July replaced with 31 August for non-audit business cases.

- New reporting introduced for presumptive income of non-residents under specified sections.

- In Schedule OS:

- Specific classification of interest income (companies/NBFC/HFC)

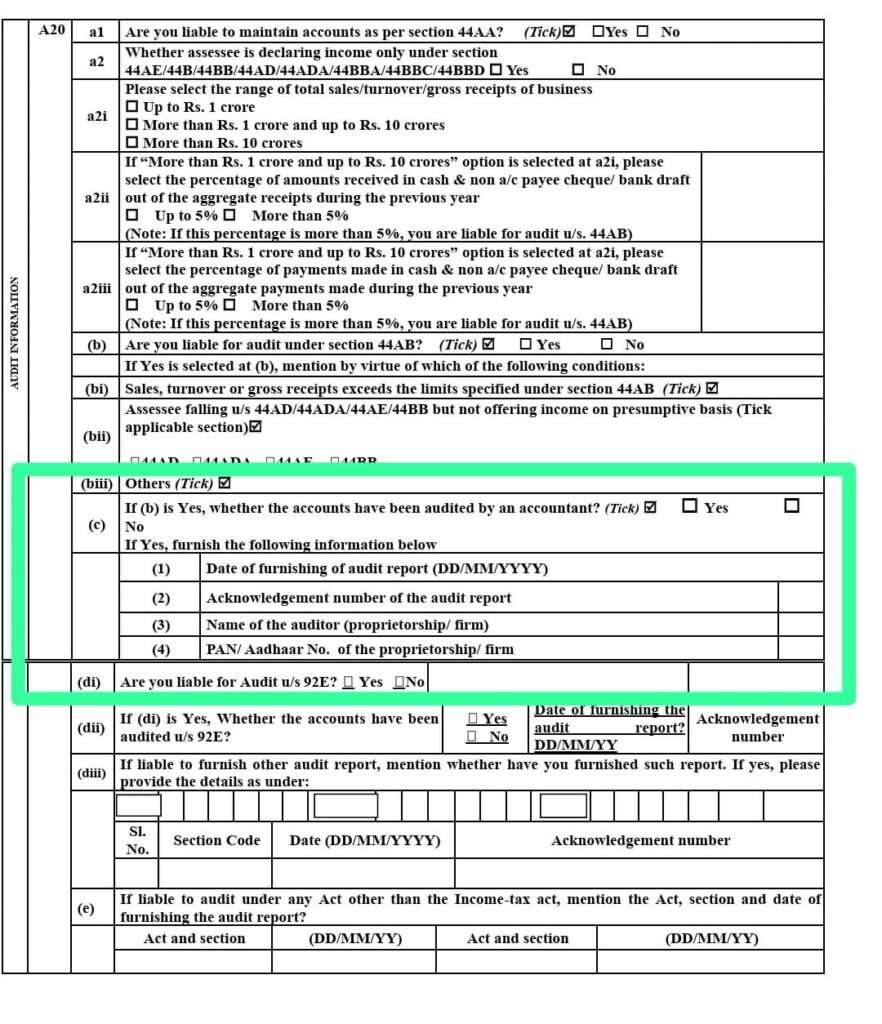

- Auditor details simplified:

- Only key fields retained (date, acknowledgement no., name, PAN)

- Capital gain bifurcation removed (simplification).

- New column for interest taxable at concessional rate (9%).

- Introduction of secondary address and simplified representative assessee details.

🔹 ITR-4 (Sugam – Presumptive Income)

- A significant change introduced in Financial Particulars:

- Taxpayer must now disclose amount of investments made

- Additional important requirement

- Mandatory disclosure of closing balance of bank account in financial particulars

- Reporting of fee under section 234I introduced.

- Changes in Section 80G & 80GGC:

- IFSC and transaction details required

- Political party name and PAN mandatory

- Major relaxation similar to ITR-1:

- Now taxpayers can report up to 2 house properties (earlier only 1 allowed)

- Removal of foreign retirement account reporting fields

- Simplified representative assessee details

- Introduction of secondary address

🔥 Key Practical Highlights (Very Important)

- Increased focus on traceability of transactions (donations, political contributions)

- Strong compliance push on:

- MSME payments

- F&O transactions

- Presumptive disclosures

- Big relief for small taxpayers:

- ITR-1 & ITR-4 now allow 2 house properties

- Data transparency increased:

- Investment disclosure

- Bank balance disclosure (ITR-4)

- Simplification measures:

- Capital gains reporting eased

- Auditor details reduced

- Removal of irrelevant disclosures

Visit www.cagurujiclasses.com for practical courses