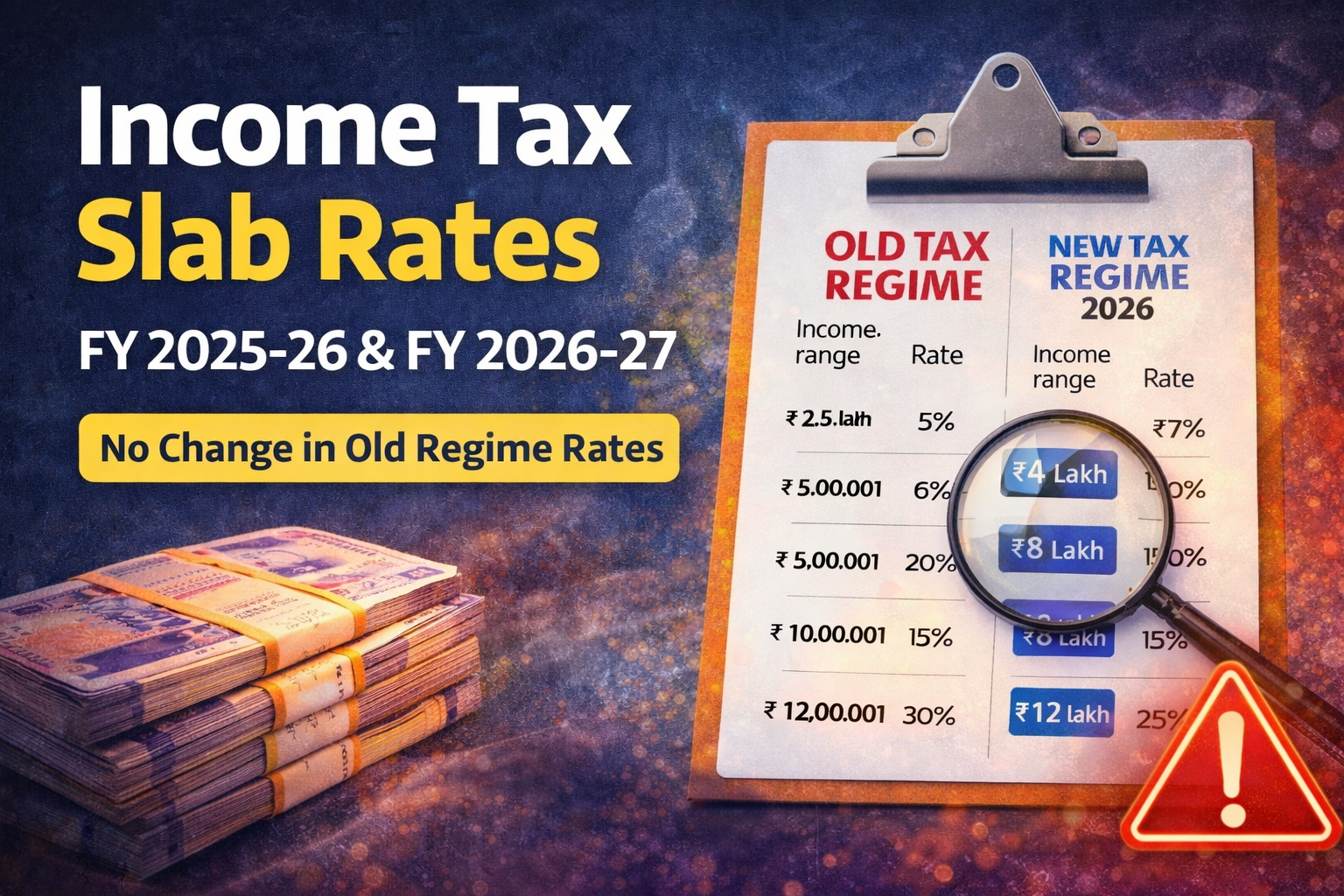

Income tax slab rates play a very important role in determining how much tax an individual or business entity needs to pay in India. With the beginning of every financial year, taxpayers often expect changes in the tax slabs announced in the Budget.

For the financial years 2025-26 and 2026-27, the Government has not made any change in the slab rates .

In this article, we will understand the income tax slab rates applicable for FY 2025-26 and FY 2026-27, including rates for individuals, companies, firms, cooperative societies and other entities.

1. Income Tax Slab Rates for Individuals (Old Tax Regime)

These slab rates apply to:

• Individuals

• Hindu Undivided Families (HUF)

• Association of Persons (AOP)

• Body of Individuals (BOI)

• Artificial Juridical Persons

There is no change in slab rates for FY 2026-27 compared to FY 2025-26

Individuals (Below 60 Years)

| Income Range | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Resident Senior Citizens (Age 60 – 80 Years)

| Income Range | Tax Rate |

|---|---|

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Resident Super Senior Citizens (Age 80+)

| Income Range | Tax Rate |

|---|---|

| Up to ₹5,00,000 | Nil |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

2. Rebate under Section 87A (Old Tax Regime)

A resident individual whose total income does not exceed ₹5,00,000 can claim a rebate under Section 87A.

Maximum rebate available:

₹12,500 or tax payable, whichever is lower.

This rebate is deducted before calculating Health & Education Cess.

3. New Tax Regime Slab Rates (Section 115BAC)

The new tax regime is the default regime for individuals, HUF, AOP, BOI and AJP.

However, taxpayers need to forgo most exemptions and deductions in order to avail the lower tax rates.

New Tax Regime – Slab Rates

From Assessment Year 2026-27, the Government has revised the slabs under the new tax regime.

| Income Range | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Rebate under Section 87A (AY 2026-27 & AY 2027-28)

If income is up to ₹12,00,000, rebate available:

Maximum ₹60,000

Meaning many taxpayers may effectively pay zero tax up to ₹12 lakh income under the new regime.

4. Surcharge on Income Tax

Surcharge applies when total income exceeds specified limits.

| Income Range | Surcharge |

|---|---|

| ₹50 lakh – ₹1 crore | 10% |

| ₹1 crore – ₹2 crore | 15% |

| ₹2 crore – ₹5 crore | 25% |

| Above ₹5 crore | 37% |

Important points:

• Maximum surcharge on certain capital gains and dividend income is 15%

• Marginal relief is available when income slightly exceeds these thresholds.

5. Health and Education Cess

After calculating tax and surcharge, Health and Education Cess is charged at 4% on the total tax liability.

6. Alternate Minimum Tax (AMT)

Individuals or HUF may be required to pay Alternate Minimum Tax (AMT) if:

Tax payable under normal provisions is less than 18.5% of adjusted total income.

In such cases, tax will be payable at:

18.5% of adjusted total income

For IFSC units earning in foreign currency, AMT rate is 9%.

Note:

If a taxpayer opts for the new tax regime (Section 115BAC), AMT provisions do not apply.

7. Tax Rate for Partnership Firms (Including LLP)

Partnership firms and LLPs are taxed at a flat rate.

| Particular | Tax Rate |

|---|---|

| Income Tax | 30% |

| Surcharge | 12% (if income exceeds ₹1 crore) |

| Health & Education Cess | 4% |

Marginal relief is available if income exceeds ₹1 crore.

8. Tax Rates for Domestic Companies

| Company Type | Tax Rate |

|---|---|

| Turnover up to ₹400 crore | 25% |

| Other domestic companies | 30% |

Surcharge

| Income Level | Surcharge |

|---|---|

| ₹1 crore – ₹10 crore | 7% |

| Above ₹10 crore | 12% |

Minimum Alternate Tax (MAT)

MAT rate for domestic companies:

15% of book profit

9. Special Corporate Tax Regimes

| Section | Tax Rate |

|---|---|

| Section 115BA | 25% |

| Section 115BAA | 22% |

| Section 115BAB | 15% |

Companies opting for 115BAA or 115BAB:

• MAT not applicable

• Surcharge fixed at 10%

10. Tax Rate for Foreign Companies

| Type of Income | Tax Rate |

|---|---|

| Royalty / Technical services (old agreements) | 50% |

| Other income | 35% |

Surcharge

| Income | Surcharge |

|---|---|

| ₹1 crore – ₹10 crore | 2% |

| Above ₹10 crore | 5% |

Plus 4% Health & Education Cess.

11. Tax Rate for Co-operative Societies

| Income Range | Tax Rate |

|---|---|

| Up to ₹10,000 | 10% |

| ₹10,000 – ₹20,000 | 20% |

| Above ₹20,000 | 30% |

Alternative tax regimes are also available:

| Section | Tax Rate |

|---|---|

| Section 115BAD | 22% |

| Section 115BAE (manufacturing co-ops) | 15% |

These regimes require forgoing certain deductions and exemptions.

For FY 2025-26 and FY 2026-27, there is no change in income tax slab rates under the old tax regime.

However, the new tax regime has been revised from Assessment Year 2026-27, with higher basic exemption limits and increased rebate thresholds.

Taxpayers should carefully compare both regimes and choose the one that results in lower tax liability based on their deductions, investments and income structure.

Disclaimer

The contents of this article are for general informational purposes only and are intended to provide quick access to tax rate information. Readers are advised to verify the provisions with the Income-tax Act, relevant rules, notifications, and official government sources before making financial decisions.

Visit www.cagurujiclasses.com for practical courses