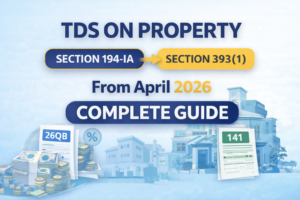

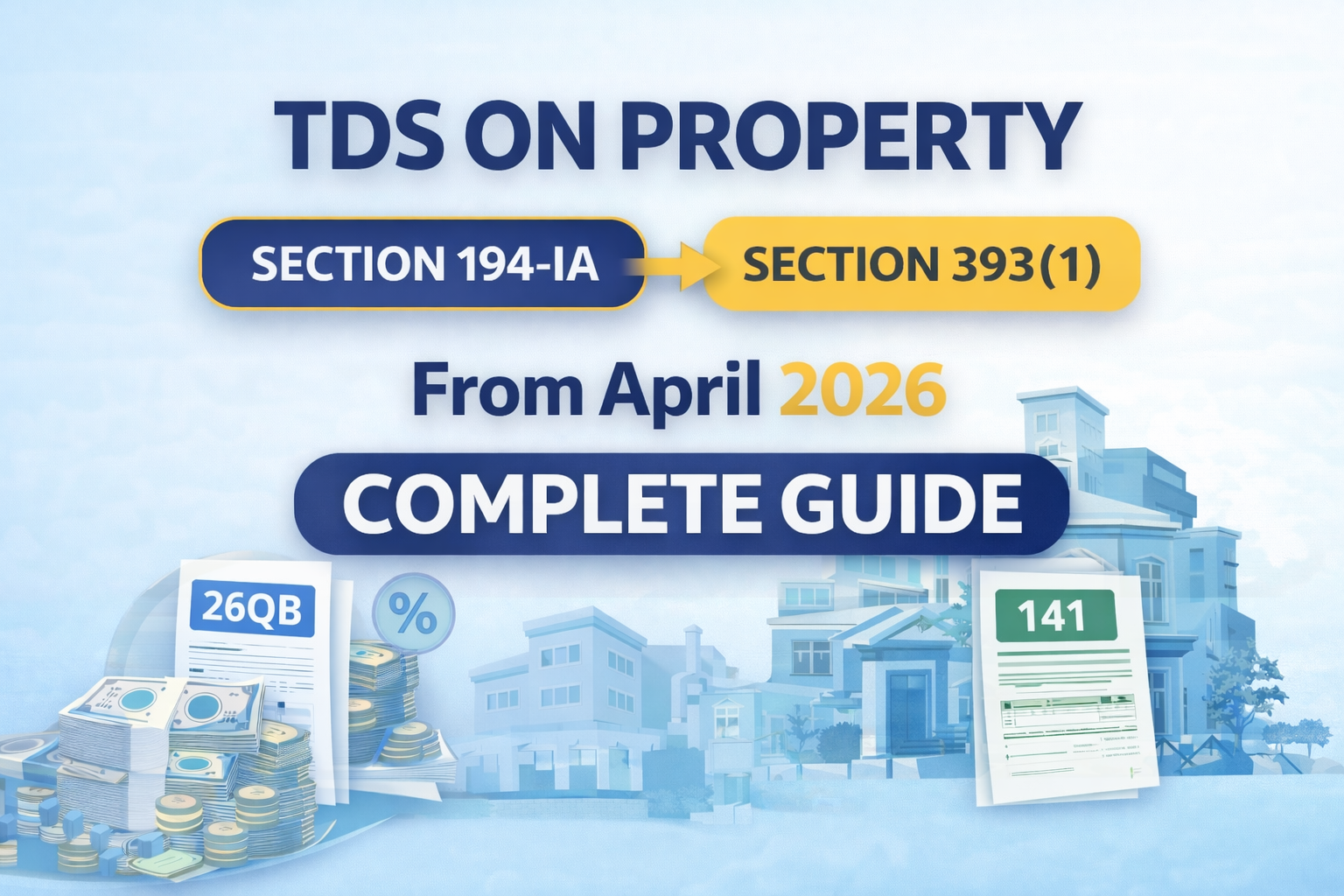

The provisions relating to Tax Deducted at Source (TDS) on purchase of immovable property have undergone a significant change with the introduction of the new Income Tax Act, 2025. Earlier governed by Section 194-IA of the Income Tax Act, 1961, these provisions will now be covered under Section 393(1) with effect from 1 April 2026. While the core concept remains largely the same, the compliance framework, including forms and procedural aspects, has been restructured. It is therefore essential for taxpayers, buyers, and professionals to clearly understand the applicability, rate, and compliance requirements of TDS on property transactions.

TDS on property is applicable when any person purchases immovable property, being land or building or part of a building, for a consideration of ₹50 lakh or more. This provision applies to both residential and commercial properties; however, agricultural land is specifically excluded. The threshold limit of ₹50 lakh is to be considered with respect to the total value of the property and not individual payments or instalments. Therefore, even if payments are made in parts, once the aggregate value exceeds ₹50 lakh, TDS provisions become applicable.

The rate of TDS under this provision is 1% of the sale consideration. However, in cases where the seller does not furnish a valid Permanent Account Number (PAN), the rate of TDS may increase significantly, generally up to 20%, as per the provisions relating to higher deduction in absence of PAN. It is therefore crucial to ensure that the seller’s PAN is correctly obtained and verified before making any payment.

One of the most important aspects of TDS on property is the timing of deduction. As per the law, TDS is required to be deducted at the time of payment or credit, whichever is earlier. In practical terms, this means that even advance payments or instalments made to the seller will attract TDS. This principle becomes particularly relevant in cases where property transactions span across different financial years, especially around the transition period of the new law effective from April 2026.

With respect to compliance, there has been a notable change in the form used for reporting and depositing TDS. Up to 31 March 2026, TDS on property is to be deposited using Form 26QB. However, for transactions on or after 1 April 2026, the new Form 141 has been introduced under the revised law. This form is required to be filed online within 30 days from the end of the month in which TDS is deducted. Taxpayers must ensure that the correct form is selected based on the date of payment, as the applicability of the form is linked to the date on which TDS liability arises.

In situations where the agreement for purchase of property is executed before March 2026 but the payment is made after April 2026, the determining factor for form selection will be the date of payment. Since TDS liability arises at the time of payment or credit, any payment made on or after 1 April 2026 will require compliance under the new provisions, and accordingly, Form 141 should be used. Conversely, payments made before this date will continue to be governed by the old system and require filing through Form 26QB. In cases involving multiple instalments, it may be necessary to comply with both forms for different portions of the same transaction.

In transactions involving multiple buyers or sellers, the applicability of TDS is determined with reference to the total property value and not the individual share of each party. This means that even if the share of each buyer or seller is below ₹50 lakh, TDS provisions will still apply if the total consideration exceeds the threshold. Additionally, separate compliance may be required for each buyer-seller combination, which increases the importance of accurate reporting.

The responsibility for deduction and deposit of TDS lies entirely with the buyer of the property. The buyer is required to deduct the tax at the applicable rate, deposit it with the government within the prescribed time, and file the relevant form. After filing, the buyer must also ensure that the TDS certificate is generated and provided to the seller. Under the earlier system, this was issued in Form 16B, and similar structured certificates are expected to continue under the new regime.

Non-compliance with TDS provisions can result in significant consequences. Interest may be levied at 1% per month for failure to deduct tax and 1.5% per month for failure to deposit the deducted tax. Additionally, late filing of the TDS statement attracts a fee of ₹200 per day, subject to the amount of TDS. Therefore, timely compliance is essential to avoid unnecessary financial burden.

In conclusion, while the fundamental principle of TDS on property remains unchanged, the transition to the new Income Tax Act, 2025 has introduced changes in section numbering and compliance forms. The key takeaway for taxpayers and professionals is that TDS applicability depends on the timing of payment, and accordingly, the correct form—Form 26QB or Form 141—must be selected. Proper understanding and execution of these provisions will ensure smooth compliance and avoid penalties.

Visit www.cagurujiclasses.com for practical courses